BOURSE SECURITIES LIMITED

October 17th, 2016

Forecasting the T&T stock market

Many investors have been inquiring as to the fortunes of the stock market in the coming year, driven by concerns to the economy and its effects on their equity portfolios. This week we at Bourse consider the outlook for the Trinidad & Tobago stock market in the context of a more challenging economic environment.

We outline some of the headwinds to corporate performance (in particular earnings), as well as some key factors which could influence stock performance. Finally, we provide some perspective on the All T&T Index – which measures the performance of listed companies registered in Trinidad & Tobago – with particular emphasis on the largest sector components.

Headwinds to Corporate Performance

By the numbers, it would appear that domestic consumption is on a downward trend. As mentioned in our recent articles focusing on the economy and national budget, real GDP growth for the Trinidad and Tobago economy is expected to be -2.3% in 2016, following negative growth of -0.6% a year before. The well-documented declines in production within the energy sector, as well as prices of its related commodities, have contributed to this anaemic growth.

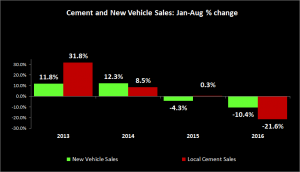

A closer look at consumer-related spending indicators over the period January to August provides some evidence of a marked slowdown in activity. Local cement sales, for example, have fallen 21.6% year-to-date in 2016 (361,820 tonnes) relative to 2015 sales of 461,664 tonnes. New vehicle sales, another barometer of consumer activity, have also declined 10.4%. A total of 10,424 new vehicles were sold between January to August 2016, as compared to 11,640 units in the corresponding 2015 period.

The latest available employment data suggests a contracting job market, with the unemployment ratio increasing to 3.8% as at March 2016 from 3.5% in December 2015 or an additional loss of 1,800 jobs. This trend is likely to continue, as businesses may not require as large a workforce in a sluggish economic environment. Other factors, such as currency availability, depreciation and associated import inflation could also provide some challenges to corporate performance.

New fiscal measures could also impact the earnings of listed Trinidad & Tobago companies. Specifically, changes to the tax regime where companies earning over TT$1M will be taxed at a marginal rate of 30% could lead to an estimated decrease in earnings by companies on the composite index of around 4% (all other factors held constant). The effects of economic slowdown are already being manifested in the stock markets, with the All T&T Index down 6.6% year-to-date. The Composite Index, which has benefited from its inclusion of several cross-listed stocks, appreciated 1.0% year-to-date.

Stock Market Drivers

Given the challenges face by companies to preserve their earnings, the anticipation of declining corporate profits would be expected to drive the stock market lower. Several non-earnings related factors, including investor confidence, could also impact the direction of the stock market.

In the first instance, stock liquidity may play a part in arresting the decline in prices of certain stocks which trade less frequently due to their closely-held nature. In such a case the relative scarcity of stocks of this nature – regardless of potentially weaker earnings – could provide some protection from purely valuation-driven price declines.

Secondly, investors contemplating an exit from stocks might consider the opportunity cost of such a move. A particular challenge for the TT dollar investor is the relative dearth of investment options. In a low interest rate, investment-starved environment, the stock market may still appeal to investors relative to current alternatives (TT dollar bonds, bank deposits etc.)

Finally, companies with the capacity to do so could preserve the absolute dividends paid to and confidence of investors in an environment of lower earnings. In particular, companies with healthy cash flows and low dividend pay-out ratios could return a higher percentage of their earnings to shareholders (that is, boost their dividend pay-out ratio) to maintain dollar dividends paid. In doing so, these companies could defend the dividend yield enjoyed by investors.

Where could the market go?

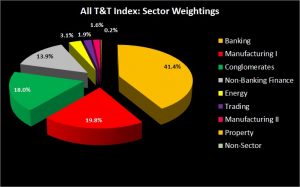

With the above economic and stock market drivers in mind, we at Bourse considered what the All T&T Index could like over the next twelve months. This involved a closer review at each of the sectors of the index and their major constituents, that is, the stocks which make up the largest part of the index. We offer below our preliminary forecast of the market’s direction, which will undoubtedly evolve as new information becomes available.

Having already declined 6.6% year-to-date, the index is projected to fall 4% – 5% over the next 12 months.

Sector Outlook

Banking. For 2016 thus far, commercial banks’ performance has been good, with the banking sector (FIRST, SBTT, RFHL) benefitting from higher average prime lending rates has increased (9.08% in October 2016versus 8.70% in October 2015). Looking ahead, probable slowing consumer and business loan demand, as well as uncertainty regarding loan-loss experiences, are expected to negatively affect the banking sector. Importantly, the banks – like all other businesses earning over TT$1M per year – will face higher corporate taxes. The sector is expected to decline around 4.5-5.0% over the next twelve months.

Manufacturing I and II. The Manufacturing I and II sectors are projected to decline 6.7% and 2.7% respectively. Higher corporate taxes and waning consumer demand, coupled with increased difficulty in accessing USD, is expected to present challenges to these sectors. Included in the Manufacturing I sector are AHL and WCO, who products will face taxes which may provide a direct deterrent to sales.

Conglomerates. Lower consumer activity and higher corporate taxes should negatively impact earnings performance. Importantly for investors, locally-based conglomerates MASSY and AMCL currently have low dividend payout ratios (average 32%), suggesting there is room to temporarily preserve cash flows to investors (dividends) amidst economic challenges. The sector is expected to decline 4.1%.

Non-Banking Finance. Including stocks such as NEL, GHL and AMBL, the sector is projected to decline 1.6%. Factors influencing corporate performance in this sector include lower energy commodity prices and local production (in the case of NEL), although this is expected to improve over the next 12-18 months. Lower consumer demand for discretionary goods (consumer-related insurance products) also played a role in the outlook for this sector, as well as higher corporate taxes.

Energy, Trading and Property. The Energy sector’s sole constituent, NGL, has a 39% stake in Phoenix Park Gas Processors Ltd (PPGPL). A projected improving outlook for natural gas production, as well as more stable prices of its products (natural gasoline, butane and propane) support NGL’s valuation. NGL also offers the highest dividend yield on the local stock exchange of 6.35%. A potential development which could impact NGL’s share price would be the divestment of NGC’s 51% holding in the company.

The Trading sector is projected to decline 3.5%. Stocks in this sector – including AGL, PHL and LJWB – will confront challenges including lower consumer demand and higher corporate taxes. The Property Sector, comprising PLD, is expected to advance 4.9%. While facing headwinds such as higher corporate taxation, the announcement of higher taxes on air freight imports are likely to benefit containerized cargo operations as businesses and individual may be incentivized to shift freight preferences.

Investor implication

With the projection of an overall decline in the local market index, how can investors better position their portfolios to minimize their investment risk and/or maximize potential opportunities?

In the first instance, highly risk-averse investors with some exposure to stocks and a short investing time horizon might consider shifting out of the asset class for now, moving to the relative safe haven of money market mutual funds or other similar instruments.

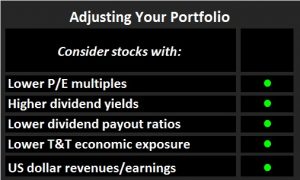

Investors who are more risk-tolerant and with longer investment horizons (in other words, willing to stay invested in stocks) may consider it worthwhile to engage in some reallocation of their portfolio. Shifting out of stocks with relatively high valuations (high price/earnings multiples), high dividend payout ratios and/or low dividend yields may be a start. On the other hand, adding companies with attractive dividend yields, low P/E multiples and low dividend payout ratios may be more value-adding to a portfolio.

Finally, investors should also consider factors such as (i) the exposure of a stock to the Trinidad & Tobago economy and (ii) stocks with significant hard currency (US dollar) earnings generation in adjusting their portfolios to mitigate the effects of a local economic slowdown. As always, it makes sense for investors to consult with a trusted and experienced advisor, such as Bourse, to help make better-informed investment decisions.

For the detailed report and access to our previous articles, please visit our website at: https://bourseinvestment.com. For more information on these and other investment themes, please contact Bourse Securities Limited, at 628-9100 or email us at invest@boursefinancial.com.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”