BOURSE SECURITIES LIMITED

30th December, 2019

AMCL, GKC Flat

This week, we at Bourse review the financial performance of two companies within the Conglomerate sector – Ansa McAl Limited (AMCL) and GraceKennedy Limited (GKC), for the nine-month (9M) period ended 30th September, 2019. Excluding certain-one off costs, AMCL delivered marginally higher profits, while GraceKennedy’s financial performance remained relatively flat. We take a closer look at the results and give a brief outlook.

Ansa McAl Limited

Ansa McAl Limited (AMCL) reported an Earnings per Share (EPS) of $2.10 at the end of third quarter 2019, a 6.7% decline from $2.25 earned in the same period last year. However, this decline included a $25M one-off cost from restructuring initiatives.

Revenue amounted to $4.72B for 9M 2019, up 3.6% or $164.8M from the prior comparable period. However, Operating Profit fell 6.6% YoY moving from $661.3M in 9M 2018 to $617.5M in 9M 2019. AMCL also recorded a $6.5M or 32.6% YoY decrease to its Share of Results of Associates and Joint Venture Interest. Resultantly, Profit Before Tax, amounted to $592.6M a 7.7% decline from $642.2M recorded last year. The Group’s effective tax rate fell from 29% to 25%. Reported profit for the period fell 2.7% YoY to $442.4M. Adjusted for one–off items, profit for the period increased approximately 2.8%.

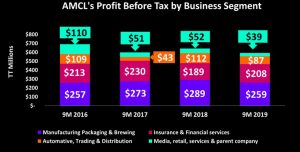

AMCL’s Manufacturing, Packaging and Brewing segment reported a 10.4% YoY decline, likely impacted by restructuring initiatives within the division.

Insurance and Financial Services, which contributes approximately 31% of AMCL’s overall Profit Before Taxation, experienced growth over the course of 9M 2019, advancing approximately 9.8% YoY. AMCL’s recent move to acquire Bank of Baroda in Trinidad and Tobago and Trident Insurance Company Limited in Barbados provides a stronger platform for growth in this segment.

The Bank of Baroda acquisition by ANSA Merchant Bank Limited (82.5% owned by AMCL), has the potential to improve AMCL’s overall profitability and signals an increased commitment to T&T by the Group. AMCL’s wide range of businesses and strong relationships with clients and employees create an environment for its commercial banking entrance – once approved – to benefit.

At the end of 9M 2019 AMCL’s Automotive, Trading and Distribution experienced some decline, falling 22% YoY, owing to adverse economic conditions within operating jurisdictions.

The Bourse View

At a current price of $55.00, AMCL trades at a trailing P/E of 16.2 times, above the Conglomerate sector average of 14.0 times. The stock offers investors a trailing dividend yield of 3.3%, in line with the sector average of 3.0%. On the basis of continued growth initiatives and fair valuations, but tempered by subdued economic conditions in AMCL’s primary markets, Bourse maintains a NEUTRAL rating on AMCL.

GraceKennedy Limited (GKC)

GraceKennedy Limited (GKC) reported Earnings per Share (EPS) of TT$0.17 for the nine months ended 30th September, 2019, representing a 6.3% improvement from TT$0.16 for the prior comparable period.

Total Revenue increased 4.3% from TT$ 3.7B in 9M 2018 to TT$3.9B in 9M 2019. The Group incurred an increase in Non-Operating Expenses owing to the adoption of a new accounting standard IFRS 16 as well as the previously adopted IAS 19 post employment benefit expenses. Overall, Total Expenses rose 3.5% to TT$ 3.8B in 2019. Other Income for the period stood at TT$ 97.7M, 15% down from the previous year. Resultantly, Profit Before Tax (PBT) gained 2.7% Year on Year (YoY), amounting to TT$244.5M. The Effective Tax Rate moved from 21% to 23% resulting in a Taxation Charge of TT$56.2M. Overall, Net Profit attributable to owners increased marginally by 1.7% from TT$163.1M to TT$165.9M.

Outlook

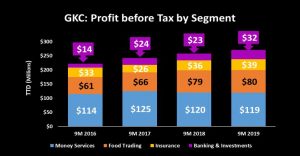

GKC’s overall PBT has consistently improved over the four-year period for 9M 2016 to 9M 2019, with the Money Services segment representing the largest contributor to PBT. In 2019 the Money Services segment PBT stood at TT$119M, a marginal 1% decline from 2018 as volatility within the Jamaican foreign exchange market impacted performance. The Group continues to unroll initiatives to improve its service via digital offerings including a digital money platform. GKC’s Food Trading segment increased 2% YoY to TT$80M.The Group commissioned a new distribution facility in the US, which is expected to increase operating efficiencies. The Insurance segment’s PBT has continuously trended upwards from 9M 2017 to 9M 2019, reporting an 8% YoY increase in 2019. PBT generated from Banking and Investments reported a 38% increase YoY, with GKC’s First Global Bank (FGB) unit doubling the number of bank agents in Jamaica from four to eight locations. The expanded distribution network is expected to improved loan growth, particularly to Small and Medium Enterprise clients.

The Bourse View

At a current price of $3.90, GKC trades at a Trailing Price to Earnings ratio of 15.1 times, above the Conglomerate’s sector average of 14.0 times. The stock also offers a Trailing Dividend Yield of 2.0%, below the sector average of 3.0%. On the basis of US dollar dividend payments, but tempered by a low trailing dividend yield and relatively muted growth, Bourse maintains a NEUTRAL rating on GKC.

For more information on these and other investment themes, please contact Bourse Securities Limited, at 226-8773 or email us at invest@boursefinancial.com.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”