BOURSE SECURITIES LIMITED

22nd May, 2017

SFC, MASSY Push Ahead

This week, we at Bourse review the latest financial results of Sagicor Financial Corporation Limited (SFC) and Massy Holdings Limited (MASSY). SFC’s market price has advanced 16.7% year-to-date, while MASSY has declined marginally by 1.0%. We highlight some key areas of the performances and provide a brief outlook on each stock.

Sagicor Financial Corporation Limited (SFC)

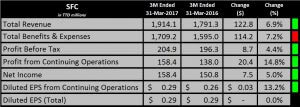

SFC reported fully diluted Earnings per Share from continuing operations of TT$ 0.29 for the first quarter ended March 31st 2017, 13.2% higher when compared to the prior period in 2016.

SFC’s Total Revenue advanced by TT$ 122.8M (6.9%). This was met by an increase in Total Benefits and Expenses of TT$ 114.2M (7.2%). The Chairman noted that higher administration costs were incurred in relation to the expansion of cards and payments business in the Jamaica segment, coupled with some other non-recurring costs in Jamaica. Profit before Tax moved from TT$ 196.3M to TT$ 204.9M. The Group’s Profit before Tax margin remained relatively stable at 10.7%, when compared to the 11.0% achieved for the same period in 2016. The Group faced a lower effective tax rate of 23% for the period (compared to the previous 30%). Overall, Profit from Continuing Operations for the period moved from TT$ 138.0M to TT$ 158.4M, an improvement of 14.8%.

Outlook

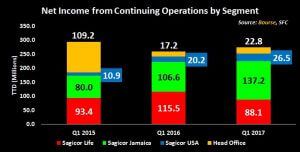

SFC’s Segment contribution has, importantly, changed considerably over time. The Sagicor Jamaica segment has overtaken the Sagicor Life segment as the top contributor to Net Income from Continuing Operations, with Net Income from Continuing Operations in its Sagicor Jamaica segment improving from TT$ 106.6M in the first quarter of 2016 to TT$ 137.2M for the same period in 2017. The Sagicor Life segment moved in the opposite direction, from TT$ 115.5M in 2016 to TT$ 88.1M in 2017. Looking ahead, the Group will need to address the decline in the Sagicor Life segment, given the overall negative impact it could have on Net Income from Continuing Operations.

The Bourse View

At a current price of $9.01, SFC offers investors a trailing dividend yield of 3.76%, above the Non-Banking Finance sector average of 3.21%. SFC trades at a trailing P/E of 6.9 times, below the sector average of 11.2 times (excluding NEL). SFC also trades at a market to book ratio of 0.74 times, below the sector average of 1.24 times (excluding NEL). Importantly for investors, SFC pays its dividends in TTD, but declares dividends in USD, providing an implicit hedge against any depreciation in the TTD. On the basis of i) continued improvements in performance, ii) a relatively low valuation, iii) an attractive dividend yield and iv) an implicit hedge against the TTD, Bourse maintains a BUY rating on SFC.

Massy Holding Limited (MASSY)

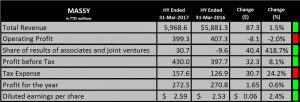

Massy Holdings Limited (MASSY) reported diluted Earnings per Share (EPS) of $2.59 for the six months period ended March 31st 2017, an improvement of 2.4% when compared to the EPS of $2.53 earned in the corresponding period in 2016. Total Revenue increased 1.5%, while Operating Profit declined by 2%. Operating Profit Margin declined from 6.9% to 6.7%. MASSY also generated $30.7M from Share of results of associates and joint ventures, as opposed to a net loss in this line item for the prior comparable period. Consequently, Profit before Tax rose to $430M, an increase of $32.3M. Taxation expense grew by $30.7M, due to an increase in effective tax rate from 32% to 36%. As a result, Profit after Tax grew marginally from $270.8M to $272.5M.

Outlook

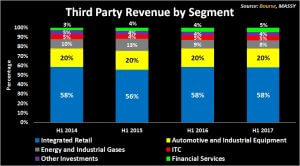

The Integrated Retail segment, MASSY’s largest business segment, has remained stable in recent years. This segment in most years has accounted for 45 percent of Profit before Tax and 58 percent of Third Party Revenue. Acquisitions in March 2017 of car dealerships in Colombia could improve the revenue generation in MASSY’s Automobile and Industrial Equipment segment, while also providing further geographical diversification. This could prove important to the Group’s performance, given that new car sales in the Trinidad and Tobago remain sluggish. New vehicle sales in T&T declined in the first quarter of this year by 25.5% compared to the same period in 2016.

On May 1st 2017, the Telecommunications Services of Trinidad and Tobago signed an agreement with Massy to acquire 100% of the shares of Massy Communications for $255 million. The sale of Massy Communications, should improve the performance of the Information Communication and Technology segment moving forward through expense reduction in subsequent periods.

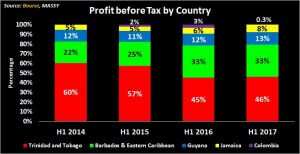

MASSY’s has operations in Colombia and various Caribbean countries. This forms part of MASSY’s diversification strategy. In the Eastern Caribbean, Guyana and Jamaica there were double-digit increases in PBT however collectively these three regions accounted for 30% of total PBT (excluding from Head Office and Other adjustments). Operations in Trinidad and Tobago and Barbados accounted for 69% of total PBT in 2017. Growth in PBT in these territories were 8.33% and 0.68% respectively, well below the profitability levels MASSY generated in other markets. With both the T&T and Barbados territories expected to face some headwinds in the near-term, MASSY’s geographic diversification initiatives, among other efforts, may play a greater role in determining the Group’s financial performance.

The Bourse View

At a current price of $51.48, MASSY trades at a trailing P/E of 10.05 times, below the Conglomerate sector average of 13.85 times. Its market to book ratio is 1.03x, which is below the sector average of 1.25x. MASSY declared an interim dividend of $0.52 per share payable on June 16th 2017, an increase of 2% compared to the same period in 2016. This brings MASSY’s trailing 12-month dividend yield is 4.10%, higher than the sector average of 2.79%. On the basis of relatively attractive valuations, but tempered by a more uncertain outlook in its main operating territories, Bourse maintains a NEUTRAL rating on MASSY.

For the detailed report and access to our previous articles, please visit our website at: http://www.remotestores.com

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”