HIGHLIGHTS

TCL 9M2022

- Earnings: Earnings Per Share increased from $0.07 to $0.31

- Performance Drivers:

- Improved Revenues

- Higher Margins

- Lower Financial expenses

- Outlook:

- Supply Chain Challenges

- Higher Input Costs

- Rating: Maintained at MARKETWEIGHT

WCO 9M2022

- Earnings: Earnings Per Share fell 22.4% to $0.83

- Performance Drivers:

- Reduced Revenues

- Lower Margins

- Outlook:

- Portfolio Transformation

- Rating: Maintained at MARKETWEIGHT

This week, we at Bourse review the financial performance of Trinidad Cement Limited (TCL) and West Indian Tobacco Company Limited (WCO) for the nine-month period ended September 30th, 2022 (9M2022). TCL benefitted from increased revenues and improved margins on account of higher cement sales, while WCO reported a decline in profitability impacted by company-specific headwinds. As the economy regains momentum, what might investors expect in the months ahead? We discuss below.

Trinidad Cement Limited (TCL)

TCL reported an Earnings Per Share (EPS) of $0.31 at the nine months ended September 30th 2022, up 323% from an EPS of $0.07 reported in 9M2021.

Revenue advanced 10.4% to stand at $1.55B in 9M2022, from a previous $1.41B. Cost of Sales was $1.02B, 0.4% higher than a previous $1.016B. Gross Profit within in the period increased to $533.1M, up by 36.5% from $390.6M. Operating expenses increased from $189.2M to $226.1M (19.5%). Operating Earnings Before Other Income (Net) rose 52.9% to $307.1M. Other Expenses (Net) increased 67.3% from $19.2M to $32.2M in 9M2022. Consequently, Operating Earnings increased 51.3% to $275M relative to $182M in the previous period. Financial Expenses were 50.6% lower in 9M2022 at $29.7M from $60.1M in 9M 2021. Bolstered by increased revenues and reduced costs, Earnings Before Taxation improved 102.4% over the prior year period, amounting to $245.8M. Taxation expense increased to $78.8M in 9M2022 from a prior $60.9M. As a result, Net Income for the period closed at $167.1M, $106.5M (175.8%) higher than the $60.6M recorded in prior comparable period. Net Income attributable to shareholders increased to $116.3M from $27.6M (up 321.0%).

Revenues Higher

The cement-producer which has manufacturing operations in T&T, Barbados and Jamaica reported a 10.4% increase in its Revenue, attributable to higher cement volumes sold across the Group. The Group’s revenue is mainly originated from the sale and distribution of cement, ready-mix concrete, aggregates, packaging and other construction material.

Cement, TCL’s largest segment, (9M2022: 97.7% of Total Revenue) rose 11.9% from a prior $1.36M to $1.52M. Concrete, accounting for 2.6% of Total Revenue, declined 14.6% YoY to $40M and third-party revenue from Packaging was -$4.3M for the period.

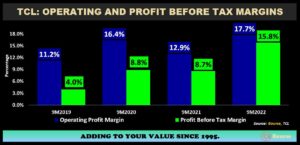

Margins Improve

TCL’s profitability has fluctuated over the years over comparable nine- month periods but has seen its largest relative improvement in both operating profit and profit before tax margin. This has been as a result of increases in sales volume across specific geographical regions and higher operating efficiency that offset inflationary costs experienced.

Operating Profit Margin expanded from 12.9% in 9M2021 to 17.7% in 9M2022, despite higher distribution and logistics expenses faced. The Profit Before Tax Margin followed suit, increasing to 15.8% from a prior 8.7%, attributable to lower financial expenses.

On August 24th, 2022, the TCL Group unveiled a US$40M capacity expansion at its Jamaican operations, Caribbean Cement Company Limited (CCCL). It is expected to increase production capacity by 30.0%, optimize heat consumption in the manufacturing process and ultimately reduce the company’s carbon footprint. The project is expected to be completed in the second half of 2024. As economic activity increases, there is a greater likelihood of improved sentiment and favourable developments for the cement producer, implying continued growth to its margins in the following periods.

The Bourse View

At a current price of $3.52, TCL trades at a market to book ratio of 1.3x and a trailing P/E ratio of 5.7 times, notably below the combined Manufacturing I & II Sector Average of 21.2 times. The Group was affected by higher input costs as a result of inflationary pressures resulting in increased fuel and shipping expenses. Consistent with the Group’s initiatives, US-dollar denominated debt in Jamaica was reduced during the period under review. On the basis of improving margins and profitability, but tempered by cost inflation and logistic challenges, Bourse maintains a MARKETWEIGHT rating on TCL.

The West Indian Tobacco Company Limited (WCO)

The West Indian Tobacco Company Limited (WCO) reported Earnings Per Share of $0.83 for the nine -month period ended September 30th 2022 (9M2022), a 22.4% decline from $1.07 reported in the prior comparable period.

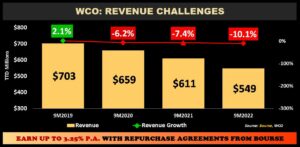

Revenue fell 10.1 % Year on Year (YoY) from $610.5M to $548.9M, followed by a 7.8% increase in Cost of Sales. Consequently, Gross Profit fell to $389.8M, 15.8 % lower compared to $462.8M reported in 9M2021. Declines in distribution costs and administrative expenses were offset by a 54.2% ($10.1M) increase in Other Operating Expenses to bring Total Expenses to $85.3M, up 6.8% YoY. Operating Profit contracted 20.5% from $383.0M in 9M2021 to $304.5M in 9M2022. Profit Before Tax declined 20.4% to $304.9M. Taxation Expense for the period decreased by 14.5% to $96.4M. Overall, WCO reported a Profit for the Period of $208.6M, down 22.8% from $270.2M reported in 9M2021.

Revenue Lower

WCO’s revenue challenges continue to persist, weighed by declining volumes of the company’s new Lucky Strike Red (formerly Du Maurier) offering. According to WCO, the company responded swiftly to the market’s reaction of its new Lucky Strike Red offering and has taken steps to address consumer preferences. The company highlighted that they have already seen progress following the re-adjustment of its product mix, in addition to growth from other brands within its portfolio.

Domestic revenue fell 13.0% to $463.1M from a previous $532.2M, while revenue from the CARICOM market advanced 9.7% to $85.8M (9M2021: $78.3M).

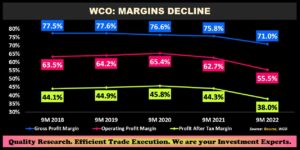

Margins Slip

WCO’s Gross Profit Margin fell from 75.8% to 71.0% in 9M 2022, following a 7.8% ($11.4M) increase in Cost of Sales likely owing to a combination of factors including higher royalties and increased costs of direct materials as stated in the previous quarter. Operating Margins fell to 55.5% in 9M 2022 relative to a prior 62.7% following a 54.2% increase in other operating expenses. Profit After Tax Margin deteriorated to 38.0% as an increase in Finance Income and a decrease in Finance Cost was offset by the company’s effective tax rate increasing from 29.4% to 31.6%.

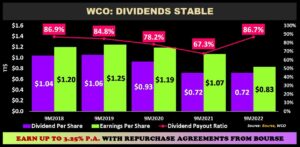

Dividends Stable

Despite a decline in earnings, WCO has rewarded shareholders with a consecutive dividend of $0.72 for the nine-month period. The company currently offers the third highest trailing 12-month dividend yield (6.2%) on the Trinidad and Tobago Stock Exchange. With stable dividends and recent margin compression, investors focusing on dividend income may increasingly view WCO as a value stock. It should be noted that the company’s trailing 12-month pay-out ratio currently stands at 107.9% which may signal a potential dividend reduction should revenue challenges persist.

The Bourse View

At a current price of $21.88, WCO trades at a P/E of 17.3 times, below the combined Manufacturing I&II sector average of 21.2 times. The company announced an interim dividend of $0.33 to be paid on November 24th 2022 to shareholders on record by November 7th 2022. The stock offers investors a trailing dividend yield of 6.2%, above the sector average of 5.5%. It should be noted that the sector average dividend yield excluding UCL’s special dividend would stand at 1.8%. While increasing inflationary pressures and lower disposable income may present additional challenges to demand, the relatively inelastic nature of tobacco products is likely to provide some support to revenue. Additionally, the company’s swift response to the market reaction of its Lucky Strike offering may lead to a rebound in demand. On the basis of relatively attractive valuations, stable dividends and narrowing margins, Bourse maintains a MARKETWEIGHT rating on WCO.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”