HIGHLIGHTS

TCL 9M2024

- Earnings: Earnings Per Share increased 30.1% from $0.32 to $0.42

- Performance Drivers:

- Higher Revenues

- Margin improvements

- Outlook:

- Uncertain economic environment

- Rating: Maintained at MARKETWEIGHT

AHL 9M2024

- Earnings: Earnings Per Share decreased 3.1% from $0.51 to $0.46

- Performance Drivers

- Lowered revenue

- Margin Reduction

- Outlook:

- Cost Management Initiatives

- New Product Offerings

- Rating: Maintained at UNDERWEIGHT

This week, we at Bourse review the performance of Trinidad Cement Limited (TCL) and Angostura Holdings Limited (AHL) for their respective nine-month periods ended 30th September 2024. TCL benefitted from higher revenues while AHL – despite growth in international markets- would have been constrained by reduced revenues and lower margins. Will TCL continue to grow earnings? Can AHL return to more stable performance, after making substantial changes to its product mix? We discuss below.

Trinidad Cement Limited (TCL)

For the nine months ended September 30th, 2024, Trinidad Cement Limited (TCL) reported an Earnings Per Share (EPS) of $0.42, up 30.1% from an EPS of $0.32 earned in the prior comparable period.

Notably, Revenue advanced marginally by 0.1% to $1.703M from a previous $1.702M in 9M2023. Cost of sales decreased by 2.5% year on year, resulting in a Gross Profit increase of 5.5% to $572.8M. Operating expenses dropped by 0.1% year on year. Operating Earnings Before Other Income grew to $346.8M from a prior $305.1M. Other Expenses climbed 44.5% to $65.4M relative to $45.3M reported in the prior period, likely driven by the significant cement kiln overhaul that occurred during the period. Resultantly, Operating Earnings increased 8.9% to $287.9M relative to $264.5M in 9M2023. Financial Expenses came in 20.9% lower, from $40.1M in 9M2023 to $31.7M in the current period. Taxation expense narrowed by 1.8% with the taxation rate declining from 26.1% to 21.8%. Earnings Before Taxation amounting to $269.2M, 17.6% higher than the prior comparable period. Resultantly, Net Income for the period settled at $210.7M, a variance of $41.4M or 24.5% higher than $167.2M reported in the prior period.

Revenues Stable

For fiscal nine-month 2024, Total Revenue saw a modest increase by 0.1% year on year, as a result of the impact of Hurricane Beryl and other adverse weather conditions in Jamaica. TCL’s revenue maintained its positive momentum for the past five (5) reporting periods.

TCL’s largest segment, Cement, which contributed 96% of Revenue fell 0.9% to $1.63B from a prior $1.65B. Concrete, accounted for 4% of Total Revenue, grew 30% YoY to $69.2M and third-party revenue from Packaging, significantly declined by 62% to $0.34M in the current period.

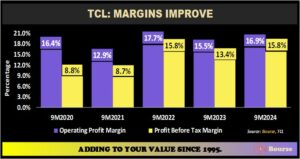

The company’s profitability margins have expanded year on year, reflecting improved performance relative to historical levels. Operating Profit Margin grew from 15.5% in 9M2023 to 16.9% in 9M2024. Similarly, Profit Before Tax Margin rose 15.8% from a prior 13.4%.

The Group’s continued emphasis on sustainability developments and adherence to its Cemex “Future in Action” program to continuously improve its top and bottom line may provide investors with confidence in the viability of its business model.

The Bourse View

TCL is currently priced at $2.61 and trades at a price to earnings ratio of 6.8 times, below the Manufacturing Sector I & II average of 9.9 times. The stock currently offers investors a dividend yield of 3.1% relative to a sector average of 4.3%. The Group resumed its dividend payments to shareholders, paying $0.08 per share in September 2024. The previous dividend payment was made in July 2017.

For the fifth consecutive reporting period, TCL continue to maintain its revenue growth. Additionally, the Group continues to pursue its environmental sustainability goals while providing modest profitability growth. On the basis of stable revenues and improved margins but tempered by an uncertain economic environment and weak investor sentiment, Bourse maintains a MARKETWEIGHT rating on TCL.

Angostura Holdings Limited

Angostura Holdings Limited (AHL), for the nine-month period ended September 30, 2024, reported an Earnings per share (EPS) of $0.46, down 9.8% compared to the previous corresponding period of $0.51.

Revenue declined 3.1% to $697.9M from the previous $720.1M, attributed to weaker performance in the local market. Cost of goods sold increased 3.2% year-on-year to $364.8M. Gross Profit fell from $366.7M to $333.2M in 9M2024 (-9.1% over prior comparable period). Selling and marketing expenses rose 5.0% to 154.1M in 9M2024 while administrative expenses edged lower 14.4% to $75.5M. Other Income was $9.7M versus an expense of $1.0M in the prior period. AHL also benefited from an expected credit loss of $0.4M versus a writeback of $0.3M in 9M2023. Results from Operating Activities amounted to $112.7M, a drop of 15.2%. Profit Before Tax (PBT) reduced to $126.5M from a previous $149.1M, down 15.2%. Resultantly, AHL’s Profit for the period closed at $94.4M, contracting $10.1M or 9.6% versus the prior comparable period.

Revenue Fall

Total Revenue contracted 3.1%, from $720.1M to $697.9M in the current period. According to AHL, revenue was lower due to a decrease in domestic sales, as the Standard Rums segment experienced a significant 8% drop year-on-year despite growth in Premium Rums and Bitters. Meanwhile, AHL reportedly showed resilience through strong growth in its international and regional markets, duty-free and co-packing segments.

AHL is focused on revenue recovery capitalizing on the growth channels like Correia’s rum line and new Angostura Chill flavors that were implemented to restore local market demand and boost sales in the Standard Rum segment.

Margins Decline

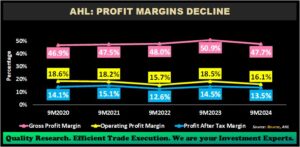

AHL’s profitability margins lowered relative to historical levels in 9M2024. AHL’s Gross Profit margin showed drop from 50.9% to 47.7%, driven by reduced revenues and higher input costs. Similarly, Operating Profit margin fell from 18.5% in 9M2023 to 16.1% in the current period, impacted by higher marketing expenses. Profit After Tax margin contracted to 13.5% compared to 14.5% in the previous period.

The Bourse View

At a current price of $16.00, down 27.1% year-to-date, AHL trades at a relatively elevated trailing P/E ratio of 23.2 times, above the Manufacturing Sector I & II average of 13.2 times. The stock offers investors a trailing dividend yield of 2.4%, below the sector average of 4.3%.

Notably, the Group continues to celebrate its 200th year anniversary in 2024 with new product releases and commemorative limited editions which will soon be available domestically and internationally. According to AHL, The Group managed to reduce overall operating expenses by 6.0%. This cost management suggests prudent financial oversight and a commitment to sustaining profitability despite revenue pressures. Investors will be monitoring for signs of revenue stabilization and sustained margins in the upcoming quarters. On the basis of lowered revenue and a decline in profitability, along with relatively high valuations, Bourse maintains an UNDERWEIGHT rating on AHL.

DISCLAIMER: “This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase, or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives, or agents, accepts any liability whatsoever for any direct, indirect, or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”