HIGHLIGHTS

RFHL FY2023

- Earnings: Diluted Earnings Per Share improved 14.8% to $10.71 from $9.33

Performance Drivers:

- Increased Net Interest Income

- Higher Credit Loss Expense

- Outlook:

- Geographical Diversification

- Rating: Upgraded to OVERWEIGHT

This week, we at Bourse review the performance of one member of the local Banking Sector, Republic Financial Holdings Limited (RFHL) for its fiscal year ended September 30th, 2023. RFHL benefitted from income improvements and its geographic diversification, leading to record earnings and financial performance. Can RFHL continue building earnings momentum into the next fiscal period? We discuss below.

Republic Financial Holdings Limited (RFHL)

RFHL reported a Diluted Earnings Per Share (EPS) of $10.71 for the twelve months ended 30th September 2023 (FY2023), a 14.8% increase when compared to the EPS of $9.33 recorded in the previous comparable period.

Net Interest Income advanced a significant 12.7% to $4.7B from the previous $4.1B, supported by robust revenue growth and increased credit advances. Other Income ticked up 9.0% to $2.14B in FY2023, relative to $1.97B in FY2022. Consequently, Operating Income increased to $6.81B, an improvement of 11.5% compared to the prior period. Despite an increase in Operating Expenses of 11.5% from $3.56B in FY2022 to $3.97B in FY2023, Operating Profit for the period amounted to $2.85B relative to $2.56B in FY2022, up 11.5%. Credit Loss Expense decreased 46.4% from $220M in FY2022 to $181M in FY2023. Profit Before Taxation (PBT) climbed to $2.60B in FY2023, 11.3% higher than $2.34B in the previous fiscal year (FY2022). Taxation Expense increased 2.46%, with the effective taxation rate moving from 27.9% in FY 2022 to 25.7% in FY2023. Resultantly, RFHL’s Net Profit attributable to Equity Holders amounted to $1.75B, 14.7% higher than $1.53B reported in the prior period.

Revenues Climb

RFHL’s Operating Income has reflected significant revenue growth over the last four (4) reporting periods and has continued to improve year on year. Net Interest Income (68.5% of Operating Income) increased 12.7% from $4.14B to $4.66B, reflecting strong consumer demand for loans evidenced by a 6.7% increase in Loans and advances ($60.7B). Conversely, Other Income (31.5% of Operating Income) grew 9.0%, partially due to increased transaction volumes as the economy rebounded particularly in Trinidad & Tobago and Barbados.

Overall, RFHL was able to improve income across its revenue streams, with Operating Income expanding from $6.10B to $6.81B in the current review period, which is broadly reflected geographically, supported by Operating Income expansion in Trinidad and Tobago (↑10.7%), Barbados (↑261.7%), Cayman Islands (↑76.3%) and Guyana (↑31.2%) operations year-on-year.

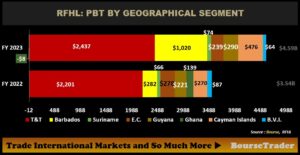

PBT Expands

RFHL was able to grow its Profit Before Tax (PBT) in five out of its eight major operating jurisdictions, advancing to $4.59B from a previous $3.54B in FY2022. Trinidad and Tobago, the Group’s largest operating jurisdiction (53.1% of PBT) expanded 10.7% YoY to $2.44B from $2.20B in the previous comparable period. Barbados, the second largest contributor of PBT (22.2%), advanced 261.7% in the period under review from $282.0M to $1.02B aided by a major credit loss recovery on financial assets. The Eastern Caribbean (5.2% of PBT) fell 14% YoY to $239M in FY2023 from $278.0M in the prior comparable period. Suriname (1.6% of PBT) climbed 12% year-on-year, moving from $66M to $74M in the current reporting period. Guyana (6.3% of PBT) recorded an increase of 31.2% from $221.0M to $290.0M. British Virgin Islands (BVI) (1.4% of PBT) contracted 26.4% YoY to $64.0M (FY2023). Ghana swung to a loss of $8M, from a profit of $138.8M recorded in fiscal year 2022.

‘Unlocked’ Shares Causing Price Volatility?

Despite record profits, RFHL’s stock price has declined 13.3% year-to-date. One of the very likely factors contributing to increased price volatility could be the liquidation of the CLICO Investment Fund (CIF), which took place in January 2023.

Prior to its closure, the CIF (through CLICO Trust Corporation Limited) would have owned and passively held –among other assets– approximately 40.07M shares of RFHL or 24.5% of RFHL. With the closure of the CIF, approximately 6.7% of total RFHL shares (or 10.98M shares) moved directly under the ownership of Corporation Sole according to RFHL’s FY2023 Annual Report, with the remaining 29.09M shares (or roughly 17.8%) moving directly into the hand of institutional and individual investors.

From another perspective, the top 10 shareholders of RFHL in FY2022 accounted for approximately 87.4% or 142.89M shares. Post-closure of the CIF, the top 10 shareholders now account for approximately 74.5% or 129.92M total RFHL shares.

The increase in ‘unlocked’ shares, particularly with more RHFL shares moving into individual accounts, could be contributing to the stock’s recent price movements. RFHL is currently trading at around its pre-COVID level, despite exceeding comparable earnings. Looking at share price movements from January 2022 to June 2023, RFHL traded within a fairly tight range between $135 to $142 per share. Subsequently, the stock has declined in near-linear fashion to the $120 range, finding some support from investors at these levels.

The Bourse View

At a current price of $120.43, RFHL trades at a trailing P/E of 11.2 times, below the Banking Sector average of 14.4 times. The company announced a final dividend of $4.10 payable on December 1st, 2023, to shareholders on record by November 16th, 2023. The stock offers investors a trailing dividend yield of 4.3%, above the sector average of 3.5%. In recent developments, RFHL announced changes to its Dividend policy, wherein the Board of Directors approved the frequency of dividends to shareholders from semi-annually to quarterly, to commence in fiscal year 2024. The group remains well positioned geographically, with its regional ‘jewel’ remaining the T&T market while building its presence in rapidly growing markets such as Guyana. Continued cautious optimism surrounding a broader regional economic recovery should bode well for banking and financial services providers.

RFHL’s combination of earnings, dividends, and current price create a relatively compelling value proposition for investors from both a capital growth and income perspective. On this basis, Bourse upgrades its rating on RFHL to OVERWEIGHT.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase, or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives, or agents, accepts any liability whatsoever for any direct, indirect, or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”