HIGHLIGHTS

RFHL Q12025

- Earnings: Diluted Earnings Per Share up 8.8% to $3.35 from $3.08

- Performance Drivers:

- Increased Net Interest Income

- Outlook:

- Geographical Diversification

- Rating: Maintained at OVERWEIGHT

FCGFH Q12025

- Earnings: Earnings Per Share increased 1.1% from $0.94 to $0.95

- Performance Drivers:

- Modest Revenue Growth

- Outlook:

- Increased Economic Activity

- Rating: Maintained at OVERWEIGHT

This week, we at Bourse review the performance of two key members of the local Banking Sector, Republic Financial Holdings Limited (RFHL) and First Citizens Group Financial Holdings Limited (FCGFH) for the three-month period (Q12025) ended December 31st, 2024. Both RFHL and FCGFH reported earnings growth, reflecting generally improving conditions. Can both banks’ performances be maintained in the coming quarters? We discuss below.

Republic Financial Holdings Limited (RFHL)

RFHL reported Diluted Earnings Per Share (EPS) of $3.35 for the three months ending December 31, 2024 (Q12025), an 8.8% increase relative to the $3.08 recorded in the previous comparable period.

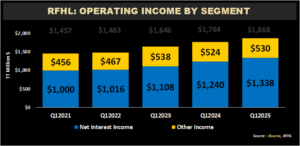

Net Interest Income grew by $98M or 7.9% year-on-year (YoY) to $1.3B. Other Income increased 1.1% to $530M in Q12025, compared to $524M in Q12024. Operating income increased by 5.9% to $1.87B. Operating expenses rose 2.8% throughout the period, from $955M in Q12024 to $982M in Q12025. The Group managed to lower its efficiency ratio moving from 54.1% to 52.6% in Q12025. Operating profit for the period was $888M, up from $811M in Q12024, a 9.5% increase. Profit before tax (PBT) stood at$824M, up 15.4% from $714M in the prior period. Taxation Expense climbed 41.4% with the Effective Taxation Rate rising from 20.3% in Q12024 to 24.9% in Q12025. Ultimately, Net Profit Attributable to Equity Holders increased by $44M, or 8.7% to $547M in Q12025.

Revenues Higher

RFHL’s Operating Income continued its upward momentum, advancing 5.9% to $1.9B in Q12025. This marked the 4th consecutive Q1 increase in quarterly income by the Group, anchored by growth in Net Interest Income. Net Interest Income (71.6% of Operating Income) advanced 7.9% from $1.2B to $1.3B. This increase was supported by continued elevated interest rates on US-related investments and growth in loans and advances as well as customer deposits. Other Income (28.4% of Operating Income) grew a more modest 1.1%.

Geographically, results broadly improved, supported by an increase in Operating Income in Barbados (↑66.9%), Suriname (↑64.4%), Guyana (↑15.2%), and Eastern Caribbean (↑2.2%) operations year-on-year.

PBT Climbs

RFHL Profit Before Tax advanced 15.4% to $824M in the period under review with six out of the eight operating territories achieving positive growth.

PBT from Trinidad and Tobago, RFHL’s primary operating jurisdiction (114.7% of PBT) declined 17.3% year-on-year to $945M from a previous $1.1B. Barbados, the second largest contributor to PBT (13.6%) advanced 300.0% from $28M to $112M in Q12025. Guyana (13.2% of PBT) recorded an increase in PBT of 29.8% to $109M in Q12025. The Cayman Islands (12.9% of PBT) declined 13.8% to $106M.The Eastern Caribbean (10.6% of PBT) advanced 42.6% from $61M in Q12024 to $87M. Suriname experienced a 160% increase in PBT YoY to $52M from $20M in the prior year quarter. Ghana recorded a gain of 11.1% in the current reporting period and British Virgin Islands (BVI) remained unchanged YoY, recording a PBT of $20M.

The Bourse View

At a current price of $113.59, RFHL trades at a trailing P/E of 9.0 times, below the Banking Sector average of 10.0 times. The Group declared an interim dividend of $0.55 per share payable on February 28th, 2025, to shareholders on record by February 19th, 2025. The stock offers investors a trailing dividend yield of 5.0%, above the sector average of 4.7%.

The Group maintains a strong outlook, driven by its diversified portfolio, solid financial performance and growth in core segments. A decline in U.S interest rates may impact Net Interest Income from the Group’s USD lending focused subsidiaries and USD denominated investments. On the basis of geographical diversification of operations, improved earnings and attractive dividends, Bourse maintains an OVERWEIGHT rating on RFHL.

First Citizens Group Financial Holdings Limited (FCGFH)

First Citizens Group Financial Holdings Limited (FCGFH) reported Earnings per Share (EPS) of $0.95 for the three months ended December 31st, 2024 (Q12025), up 1.1%, relative to $0.94 reported in the prior comparable period (Q12024).

Net Interest Income grew 2.0% from $512.2M in Q12024 to $522.4M in Q12025. Other Income expanded 6.1% from $163.1M to $173.1M. Consequently, Total Net Revenue expanded to $695.5M, up 3.0% from a previous $675.3M. Credit Impairment Losses amounted to $11.4M relative to $0.5M in Q12024. Non-Interest Expenses remained flat from $357.3M in Q12024 to $357.5M in Q12025, resulting in a 2.9% increase in Operating Profit (from $317.4M to $326.6M). The Group’s Share of Profit in Associates and Joint Ventures amounted to $4.2M, down 47.5% from a prior $7.9M. Profit before Taxation settled at $330.7M. Taxation Expense grew 2.8% to $90.8M, with the Group’s effective tax moving from 27.1% in Q12024 to 27.4% in Q12025. Overall, Profit After Taxation increased 1.2% in from $237.1M to $240.0M.

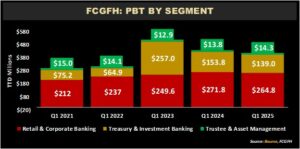

Segment Performance Lower

FCGFH reported a 4.8% year-on-year decline in segment Profit Before Taxation (PBT), excluding eliminations. Retail & Corporate Banking, the largest contributor to PBT, made up 63.3% of the total (before eliminations), decreasing by 2.6% from $271.8M to $264.8M. Treasury & Investment Banking, the second-largest contributor with 33% of PBT (before eliminations), saw a 9.6% decrease year-on-year, falling to $139.0M. The Trustee & Asset Management segment, 3.4% of PBT (before eliminations), grew by 3.6%, reaching $14.3M.

Credit Impairment Losses

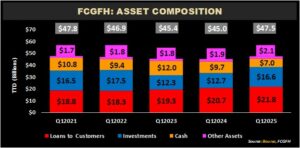

FCGFH’s Loans to Customers increased from $18.2B in Q12022 to $21.8B in the most recent period. The Group achieved a 5.1% year-on-year growth in Loans to Customers, growing from $20.7B to $21.8B. Meanwhile, credit impairment losses totalled $0.01M (approximately 0.1% of Total Loans), indicating solid lending practices and a generally favourable credit environment.

FCGFH’s total assets grew by 5.5% year-on-year, increasing from TT$45.0B in Q12024 to TT$47.5B in Q12025. Loans to Customers, which make up 45.8% of Total Assets, rose 5.1%, reaching $21.8B. Investments, accounting for 34.9% of Total Assets, totalled $16.6B, a 31.1% increase compared to the prior period. Cash and Statutory Deposits, representing 14.8% of Total Assets, fell to $7.0B. As it pertains to balance sheet trends, FCGFH has been prioritizing asset acquisitions in its loan portfolios while also increasing its investment holdings. FCGFH, as reported at its last broker meeting, has also been ‘pivoting’ its asset composition to meet anticipated future regulatory developments, which demonstrate the forward-looking nature of the Group.

The Bourse View

FCGFH is currently priced at $42.03 and trades at a P/E ratio of 11.1 times, above the Banking Sector average of 10.0 times. The Group declared an interim dividend of $0.52 per share payable on March 7th, 2025, to shareholders on record by February 14th, 2025. The stock offers an attractive dividend yield of 5.7%, well above the sector average of 4.7%.

FCGFH continues to offer quarterly dividends in line with the Group’s policy, which should attract income-focused investors. The Group also remains committed to expanding its credit portfolio to meet its broader strategic goals. Notably, FCGFH is consciously pursuing a so-called ‘hybrid’ approach to customer transactions and engagement, investing in both its online/digital services as well as its physical footprint. On the basis of improving earnings growth and attractive dividends, Bourse maintains an OVERWEIGHT rating on FCGFH.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”