HIGHLIGHTS

PHL HY2023

- Earnings: Earnings Per Share increase 84.5% from $0.17 to $0.32

Performance Drivers:

- Improving Revenue

- Improving Margins

- New Restaurant Openings

- Outlook:

- Cooling Inflationary pressures

- Geographical Diversification

- Rating: Maintained at MARKETWEIGHT

This week, we at Bourse review the financial performance of Prestige Holdings Limited (PHL) for the six-month ended May 31st, 2023. PHL benefited from higher profit margins and successful geographical expansion. We also provide an update on the upcoming maturity of the NIF bond. We discuss below.

Prestige Holdings Limited (PHL)

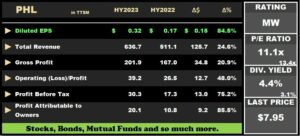

For the six months ended May 31st, 2023, Prestige Holdings Limited (PHL) reported Diluted Earnings Per Share (EPS) of $0.32, an increase of 84.5% from $0.17 reported in HY2022.

Revenue grew from a prior $511.1M in HY2022 to $636.7M in the current period, an increase of 24.6%. This performance was supported by both increased existing store and new store sales. Despite Cost of Sales increasing 26.4% from $344M to $435M in HY2023, Gross Profit still climbed 20.9% to $201.9M. Operating Expenses and Administrative Expenses went up by 8.4% and 34.6%, respectively. Other income decreased 21.6% to $0.8M. Resultantly, PHL reported Operating Profit of $39.2M in HY2023, relative to $26.5M in the prior comparable period (a 48% improvement). Finance Costs fell 2.8% to stand at $8.9M. The Group recorded a Profit Before Tax (PBT) of $30.3M, a 75.2% increase relative to the Profit Before Tax of $17.3M recorded in HY2022. Overall, PHL reported Profit Attributable to Owners of the Parent of $20.4M, rising 88.2% from $10.8M in the prior comparable period.

Revenues Higher

PHL’s revenues trajectory continued in positive fashion, supported by sales growth from existing and new restaurants. Total revenue climbed 24.6% from $511M (HY2022) to $637M in 2023, reflective of increased economic activity.

PHL successfully opened its first Starbucks restaurant in Guyana in April 2023 and is currently in the “advanced stages” for the opening of additional restaurants in the market. The company anticipates a total of 5 new locations to be opened in Trinidad and Tobago in 2023, having already opened three Starbucks restaurants for the first six months of 2023.

Margins Improve

Despite a marginal decline in PHL’s Gross Profit Margin from 32.7% in HY2022 to 31.7% in HY2023, the Group’s profitability margins generally improved. Operating Profit Margin moved from 5.2% to 6.2% in HY2023, with Operating and Administrative Expenses increasing at a slower pace relative to Gross Profit. A moderation in Finance Costs also led to better Profit Before Tax (PBT) margin, improving from 3.4% in HY2022 to 4.8% in HY2023.

Importantly, the apparent improving cost management of PHL would have taken its Operating Profit and PBT Margins to levels higher than its pre-COVID (HY2019) figures of 4.9% and 4.5% respectively. This is particularly impressive in the context of significant inflationary pressures over the past 12-18 months.

The Bourse View

PHL trades at a current market price of $7.95, up 26.6% year-to-date. The stock trades at a trailing 12-month P/E ratio of 11.1 times, below the trading sector’s average of 13.4 times. The group declared an interim dividend payment of $0.15, to be paid to shareholders on August 4th, 2023. The stock offers investors a trailing dividend yield of 4.4%, above the sector average of 3.1%. On the basis of consistent revenue growth, improving profitability margins and continued new restaurant openings, Bourse maintains a MARKETWEIGHT rating on PHL.

Bond Market Update

NIF ‘A’ to Mature

The National Investment Fund Holding Company Limited’s (NIF) 4.50% 2023 Series A bonds will mature on 9th August 2023. NIF Series A bondholders should comfortably expect to receive maturity proceeds, with Series A repayment likely funded via the issuance of a new NIF ‘Series D’. In its latest rating release on NIF, CariCRIS assigned a rating of ‘CariAA’ on the regional scale and ‘ttAA’ on the national scale for the proposed Series D of up to TT$1.2B, a value which matches the outstanding amount of Series A bonds.

NIF Market Value, Collateral Ratios solid

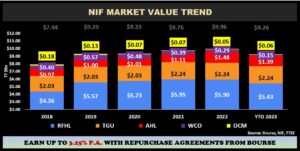

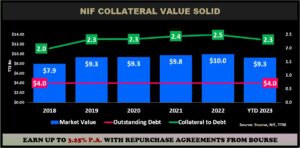

The NIF Series of Bonds amounting to TT$4.0B issued by the company in 2018 were roughly half the market value of the company at that point in time. Since issuance, the value of NIF’s underlying portfolio of assets has grown by roughly 17.0% to an estimated TT$9.3B from the initial TT$7.9B in 2018, calculated based on market value of the firm’s underlying holdings traded on the TTSE.

The face value of the bonds (TT$4.0B) represents 43.2% of the company’s portfolio market value. In other words, the market value of the firm is 2.3 times the outstanding value of debt issued by the NIF.

About the National Investment Fund (NIF)

The National Investment Fund Holding Company Limited (NIF) Initial Public Offering of bonds was offered in three tranches on August 9th, 2018; Series A, a 4.50% fixed rate bond due August 9th, 2023; Series B, a 5.70% Fixed Rate Bond due August 9th, 2030; and Series C, a 6.60% fixed rate bond due August 9th, 2038. The face value of bonds issued were TT$1.2B for Series A, TT$1.6B for Series B and TT$1.2B for Series C respectively. The underlying holdings for NIF are Republic Financial Holdings (RFHL), Trinidad Generation Unlimited (100% owned by NIF), Angostura Holdings Limited (AHL), West Indian Tobacco Company Limited (WCO) and One Caribbean Media Limited (OCM), each currently weighing 58.6%, 24.2%, 15.0%,1.7% and 0.6% respectively of the portfolio.

On June 29th, 2023 the Caribbean Information and Credit Rating Services Limited (CariCRIS) reaffirmed the ratings presently assigned to the TT$4.0B bond issue of ‘CariAA’ (Local Currency Rating) on the regional scale and ‘ttAA’ (Local Currency rating) on the Trinidad and Tobago (T&T) national scale. This indicates that the creditworthiness of this debt obligation in relation to others in the Caribbean and Trinidad and Tobago as High. Due to the expectation that the performance of the NIF’s underlying assets will remain strong over the next 12-15 months, CariCRIS has further assigned a stable outlook on both ratings.

GORTT International Credit Ratings Resilient

In recent developments, The Government of the Republic of Trinidad and Tobago’s (GORTT) credit rating outlook was recently upgraded by Moody’s Investors Services (Moody’s) from stable to positive and reaffirmed the ‘Ba2’ rating of T&T. On July 26th 2023, Standard & Poor’s (S&P) Global Ratings reaffirmed T&T’s ‘BBB-’ Investment Grade credit rating, with a stable outlook. The positive developments are based on the country’s economic and financial resilience, reflective of its overall credit strength.

DISCLAIMER: “This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase, or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives, or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”