HIGHLIGHTS

NCBFG HY 2022

- Earnings: EPS rose 83.1% from $0.11 to $0.20

- Performance Drivers:

- Increased Income from Banking and Insurance Activities

- Higher Operating Expenses

- Outlook:

- Economic Uncertainty

- Rating: Maintained at MARKETWEIGHT.

GHL Q1 2022

- Earnings: EPS increased 1.3% from $0.76 to $0.77

- Performance Drivers:

- Higher Net Income from Insurance Activities

- Decline in Net Income from Investing Activities

- Uptick in Fee and Commission Income

- Outlook:

- Volatile Financial Markets

- Rating: Maintained at MARKETWEIGHT.

This week, we at Bourse review the performance of NCB Financial Group Limited (NCBFG) for the six months ended March 31st, 2022 (HY 2022) and Guardian Holdings Limited (GHL) for the three months ended March 31st 2022 (Q1 2022). Both Groups recorded an improvement in earnings helped by higher Net Premium Income but faced headwinds caused by unfavourable financial markets. Can both Groups continue to navigate the increasingly uncertain operating environment? We discuss below.

NCB Financial Group Limited (NCBFG)

NCBFG reported Earnings Per Share of TT$0.20 for the half year ended March 31st, 2022, 83.1% higher than TT$0.11 reported in the prior comparable period.

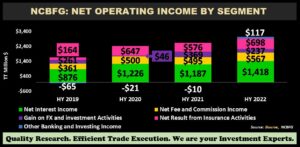

The Group’s Net Interest Income advanced 19.5% to TT$1.42B from a prior TT$1.12B. Net Fee and Commission Income increased 14.5% to TT$567.4M relative to TT$495.3M in HY 2021. Gains on FX and Investment Activities, however, fell 35.8% to TT$236.6M from TT$368.8M, attributable to more volatile financial markets. Credit Impairment Losses fell from TT$110.9M in the prior period to TT$100.6M, 9.2% lower. Net Result from Banking and Investment Activities grew 14.6% moving from TT$2.04B in HY 2021 to TT$2.34B in HY 2022, reflecting continued growth in lending, higher investment securities coupled with effective interest spread management. Net Result from Insurance Activities rose 21.0% to TT$697.5M and Commission and Other Selling Expenses increased marginally to TT$382.2M. Overall, Net Operating Income stood at TT$3.04B, 16.0% greater than the prior comparable period. Operating Expenses climbed 9.8% to $2.27B relative to a previous TT$2.06B, primarily related to the execution of ‘various strategic initiatives’ as the Group strives to enhance customers’ service experience and its digital capabilities. Operating Profit was TT$771.2M, 39.4% higher than TT$553.1M. Profit Before Tax was up 42.7% YoY to TT$792.6M as a TT$20.8M increase in Share of Profit of Associates, lent support. Taxation expense fell 18.3% to TT$123.1M. Net Profit totalled TT$669.5M, increasing 65.4% while Net Profit Attributable to Shareholders climbed to TT$457.0M from TT$258.0M, 77.2% higher.

Operating Income Higher

NCBFG reported a significant 16.0% increase in Net Operating Income for HY 2022. Net Interest Income, the largest component of Net Operating Income (46.7%), expanded 19.5% as the Group recorded strong growth in its interest earning portfolios. NCBFG’s loan portfolio and customer deposits both increased 17.0%, reflecting customers’ continued confidence in the Group.

Net Result from Insurance Activities (23.0% of Net Operating Income) rose 21.0%, driven by a 14.1% increase in Net Underwriting Income and increased net performance from life and health insurances. Net Fee and Commission Income (18.7% of Net Operating Income), climbed 14.5% to TT$567M YoY, with revenues increasing 50.0% following higher levels of transactions. Gains on Foreign Currency and Investment Activities fell 35.8% in HY 2022 from TT$369M to TT$237M, due to lower net foreign exchange gains and a fairly difficult period for financial markets. Other Banking and Investing Income increased to TT$117M in the period under review, led by gains in dividend income and other operating income.

Operating Profit by Activity

Five of NCBFG’s seven operating segments recorded year-on-year improvements. Life and Health Insurance & Pension Fund Management, which accounts for 44.3% of Operating Profit, advanced 13.7% from $515M to $585M following a rebound in economic activity. Corporate and Commercial Banking (10.2% of Operating Profit) expanded 78.5% from $75M to $134M as a result of continued growth in lending. Conversely, General Insurance contracted 65.3% primarily due to an increase in property claims.

Outlook

While the region’s prospects for recovery have strengthened given the widespread economic reopening, the operating environment continues to face elevated uncertainty from geopolitical tensions, rising inflation and interest rate movements and likelihood of tepid consumer demand. Based on NCBFG’s 2021 annual report, Jamaica remains its largest jurisdiction by Operating Income, accounting for 55%. Trinidad and Tobago is the second largest with 15%, with the Dutch Caribbean accounting for 8%, Bermuda at 5% and other at 17%.

The significant surge in inflationary pressures has forced many central banks, including the Bank of Jamaica (BOJ) and the US Federal Reserve to aggressively ‘tighten’ monetary policy to combat inflation. Other countries within NCBFG’s operating territories could follow suit in the coming months, further clouding the outlook for economic activity.

The Bourse View

NCBFG is currently priced at $6.05 and trades at a (now much more modest) price to earnings ratio of 16.7 times, relative to the Banking Sector average of 16.8 times. The stock offers investors a trailing dividend yield of 0.4%, materially below the sector average of 2.5%. While volatile financial markets may continue to generate weaker performance in its Investment Activities segment, the Group’s Insurance and Brokerage segments may be poised to benefit from improving economic activity across its operating jurisdictions. On the basis of improved performance, relatively fair valuations and turbulent financial markets, Bourse maintains a MARKETWEIGHT rating on NCBFG.

Guardian Holdings Limited (GHL)

Guardian Holdings Limited (GHL) reported Earnings per Share of $0.77 for its first quarter ended March 31st 2022, up 1.3% from $0.76 in the prior comparable period.

Net Result from Insurance Activities grew to $265.6M in Q1 2022 (up 27.7%) from a previous $208.0M. Net Income from Investing Activities contracted 8.1% to $305.5M relative to a prior $332.4M. Fee and Commission Income from Brokerage Activities advanced 10.4% to $40.5M. Collectively, Net Income from All Activities increased 6.0% during the period.

GHL recorded Net Impairment Losses on Financial Assets of $17.5M in Q1 2022, relative to $5.0M in the prior period. Operating Expenses and Finance Charges increased 7.5% and 2.5% respectively. Operating Profit stood at $210.0M, 1.1% lower relative to a prior $212.3M. Share of Profit of Associated Companies was marginally higher ending the period at $4.3M. Profit Before Taxation declined 0.8% YoY moving from $215.9M to $214.3M. Taxation Expense was down 32.1%, settling at $26.2M. Overall, Profit Attributable to Equity Holders of the Parent rose 1.9% to $179.4M, compared to a previous $176.1M.

Insurance Income Boosts Performance

Net Income from All Activities increased 6.0% during the 3-month period with two of the three segments showing improvement. Net Income from Investment Activities (50.0% of Net Income) declined 8.1%, likely attributable to declines in equity markets, higher interest rates pushing bond prices lower and generally weaker investor sentiment. According to GHL’s 2021 Annual Report, approximately 40% of the Group’s investment portfolio is measured at fair value through profit or loss, suggesting possible fluctuations in subsequent earnings as global market volatility surge.

Net Income from Insurance Activities (43.4% of Net Income) expanded 27.7% in response to increased economic activity. Gross Written Premiums advanced 4.7% ($95.2M) while Net Written Premiums climbed 6.5% ($81.6M). GHL’s Life, Health and Pensions segment recorded an 8.6% increase in Gross Premiums primarily from its Trinidad and Tobago and Dutch markets. Net Income from Brokerage Activities (6.6% of Net Income) increased 10.4% during the period to $40.5M.

GHL’s Trailing Earnings Per Share declined from $4.26 in Q1 2021 to $3.38 in Q1 2022. The Group’s Price-to-Earnings (P/E) multiple expanded from 6.0 times to 8.0 times in the current period, now comparable to its historical average P/E valuation during 2017-2019 of 8.5 times.

The Bourse View

GHL is currently priced at $27.00, having depreciated 10.0% year to date. The stock currently trades at a price to earnings ratio of 8.0 times, above the Non-Banking Finance sector average of 7.8 times. The stock currently has a trailing dividend yield of 2.6% relative to the sector average of 1.9%.

Continued market volatility due to the geopolitical tensions, higher imported inflation and tighter financial conditions may dim growth prospects regionally and weigh on GHL’s Investing Activities contribution in the short to medium term. Based on its 2021 annual report, roughly 42% of GHL’s revenue stems from Trinidad and Tobago with a further 38% coming from Jamaica and Dutch Caribbean. On the basis of fair valuations, but tempered by heightened volatility in financial markets as well as uncertain (though improving) economic conditions in GHL’s operating jurisdictions, Bourse maintains a MARKETWEIGHT rating on GHL.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”