| HIGHLIGHTS GHL 9M 2020 · Earnings: EPS up 12.4% from $1.86 to $2.09 · Performance Drivers: o Insurance Income higher amid reduced net claims and capital optimization based gains · Outlook: o Growth potential from NCBIC Acquisition and consolidation of operations o Potentially improving investing income due to sustained recovery in financial markets · Rating: Maintained at NEUTRAL. AMBL 9M 2020 · Earnings: EPS down 51.4% from $1.77 to $0.86 · Performance Drivers: o Decline in retail loan demand o Contractions of financial markets in HY 2020 o Improvements with stabilising markets in Q3 2020 · Outlook: o Potentially muted demand for merchant bank services amid adverse economic conditions o Potential growth due to gradually improving financial markets · Rating: Maintained at NEUTRAL. |

Non-Banking Finance Stocks Mixed: GHL Advances, AMBL Declines

This week, we at Bourse review the performance of Non-Banking Finance sector stocks Guardian Holdings Limited (GHL) and Ansa Merchant Bank Limited (AMBL) for the nine-month period ended 30th September, 2020 (9M 2020). GHL reported improved earnings, bolstered by increases in its insurance income segment. AMBL, on the other hand reported a decline in revenue, coinciding with an increase in costs ultimately weighing on its earnings. We discuss further below.

Guardian Holdings Limited (GHL)

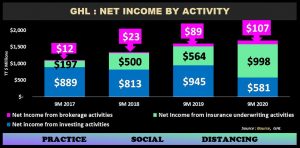

GHL reported an Earnings Per Share (EPS) of $2.09 for the nine months ended September 30th 2020 (9M 2020), up 12.4% from $1.86 in the previous comparable period. GHL benefited from a 77.0% improvement in Net Results from Insurance Activities, which for the period stood at $998.2M compared to a prior $564.05M. Net Income from Investing Activities, which contributed 59.1% of Net Income in 9M 2019, contracted 38.6% in 9M 2020, amounting to $580.7M. Fee and Commission Income from Brokerage Activities recorded an increase of 20.1% from $88.9M to $106.8M. Consequently, Net Income from all Activities climbed 5.5% to stand at $1.69B in 9M 2020.

Impacted by adverse economic conditions, Net Impairment Losses on Financial Assets grew to $24.8M relative to $4.7M in the prior period. Operating Expenses increased 1.7%, incurring a cost of $922.8M relative to $907.0M in 9M 2019.The Group reported an Operating Profit of $628.2M, 9.0% higher than $576.6M recorded in the prior period. Share of Profit of Associated Companies declined 15.2%, amounting to $18.9M while Profit Before Taxation for the period rose 8.1%, to $647.2M. Profit attributable to equity holders of the parent stood at $485.2M, 12.2% more than $432.6M recorded in the prior year.

Insurance Activities Drive Net Income Higher

Net Income from Insurance Activities significantly drove top line growth in the period, closing at $998.2M, 77.0% greater than the prior comparable period. The upswing in Income generated by insurance activities was attributed to the reduction of natural disasters impacting the Caribbean within the period and a consequent decline in net claims, in addition to the ‘booking of capital optimisation’ arising from the acquisition of NCB Insurance Company Limited (NCBIC). GHL’s Net Income growth was supported to a lesser degree by Net Income from Brokerage Activities, reporting a 20.1% increase. The uptick in Income from Brokerage Activities was supported by inorganic growth initiatives. The jump in Net income from Insurance Activities helped to more-than-offset declines in Income from Investing Activities which, contracted 38.5% YoY, resulting from declines in local and regional equity markets.

NCBIC Acquisition

On the 30th of September, 2020 the Guardian Group effectively acquired the insurance and annuities portfolio of NCBIC. The acquisition is expected to allow for the streamlining of parent company NCB Financial Group’s insurance operations and the addition of bancassurance expertise and credibility to GHL’s service portfolio. To finance the acquisition, the Group issued J$13.4B (US$90M or TT$623M) of bonds on the Jamaican market, which is estimated to add a gross annual TT$42M in interest costs. At the end of Q3 2020, GHL reported a $683.6M (27%) increase in its financial liabilities relative to Q2 2020.

The Bourse View

Currently priced at $20.15, GHL trades at a P/E ratio of 6.3 times relative to the Non-Banking Finance Sector average of 11.1 times. The stock offers investors a trailing dividend yield of 2.5%, above sector average of 1.1%. The synergies from acquisition of NCBIC and gradual recovery of financial markets is likely to provide support for GHL’s positive earnings trajectory in subsequent quarters. While the list of positives has grown, the major uncertainty remains the severity of economic fallout from the COVID-19 pandemic. Against this backdrop, Bourse maintains a NEUTRAL rating on GHL.

Ansa Merchant Bank Limited (AMBL)

AMBL reported an Earnings Per Share of $0.86 for the nine-month period ended 30th September 2020 (9M 2020), 51.4% lower than the $1.77 reported in the previous period. Total Income contracted 6.8%, from $742.1M in 9M 2019 to $691.8M in 9M 2020. On the other hand, Total Expenses grew 10.2% YoY, to $588.3M. Resultantly, Operating Profit stood at $103.5M, declining 50.2% from the previous period (9M 2019: $208.0M). Similarly, AMBL’s Profit After Taxation (PAT) and Profit Attributable to Shareholders recorded a 51.5% reduction to $73.2M from a prior $151.1M.

Operational Segments Record Decline

In the context of muted economic activity and weaker regional financial markets, AMBL’s three operational business lines suffered a year on year decline in performance as measured by Profit Before Tax (PBT). Banking, AMBL’s largest segment, reported a 44.6% decline, delivering a Profit Before Tax of $78.6M relative to $142.0M in the prior year. Insurance Services fell 73.7% in the period under review, generating PBT of $25.7M relative to a previous $97.6M. Mutual Funds swung to a Loss Before Tax of $9.2M relative to a prior Profit of $11.8M.

Adverse economic conditions have altered the flow of disposable income within the economy and increased the likelihood of loan/debt default, driving the need for financial entities to increase loan loss provisioning. AMBL being no exception, the Group noted an increase in its IFRS 9 provisioning, a likely contributor to the 10.2% increase in the Group’s Operating Expenses despite the fall in revenue. Additionally, the Group has noted its exposure to mark to market losses resulting from financial market contractions in early 2020 and slowed recovery in regional markets.

Recovery Underway?

In the first half 2020, AMBL recorded 73.0% decline in its reported EPS relative to the prior comparable period. At the end of 9M 2020, this decrease slowed to 51.4%, highlighting some recovery over the course of Q3 2020. In Q3 2020 the Group reported a Profit Before Tax of $57M, 14% greater than that recorded in Q3 2019 as financial markets recover and economic activity slowly resumes. The easing of COVID-19 restrictions across Trinidad and Tobago could support earnings recovery, though it is too early to tell how long-lasting the impact of COVID-19 will be on AMBL and almost every other business.

On a positive note, AMBL’s acquisition of Bank of Baroda’s commercial banking operations provides a fairly attractive platform for growth, particularly in the context of its parent company’s (Ansa McAl Limited or AMCL) breadth of businesses, corporate relationships and associated banking needs.

The Bourse View

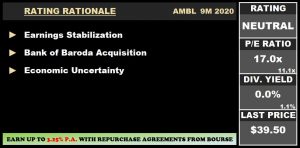

AMBL is currently priced at $39.50 and trades at a price to earnings ratio of 17.0 times, above the Non-Banking Finance Sector average of 11.1 times. This is largely a result of AMBL’s sharp decline in earnings, combined with the 10.2% advance in price year-to-date. The Group’s decision to forego payments of a final FY2019 dividend and interim dividend for 2020 means its trailing dividend yield stands at 0% relative to a sector average of 1.1%. On the basis of anticipated earnings recovery and eventual operationalization of its newly-acquired commercial banking franchise, but tempered by an outlook still clouded largely by COVID-19, Bourse maintains a NEUTRAL rating on AMBL.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”