HIGHLIGHTS

FCI FY2023

- Earnings: Earnings Per Share 51.8% higher, from TT$0.74 to TT$1.12

- Performance Drivers:

- Higher Revenues

- Higher Interest Rates

- Outlook:

- Interest Rate Normalization

- Continued Economic Recovery

- Rating: Maintained at OVERWEIGHT

SBTT FY2023

- Earnings: Earnings Per Share 0.8% lower, from $3.88 to $3.85

- Performance Drivers:

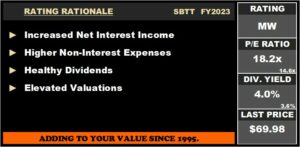

- Increased Net Interest Income

- Higher Operating Expenses

- Outlook:

- Continued Economic Recovery

- Rating: Maintained at MARKETWEIGHT.

This week we at Bourse review the performance of two locally-listed, Canadian banking giants, FirstCaribbean International Bank Limited (FCI) and Scotiabank Trinidad and Tobago Limited (SBTT) for their respective full year financial results for the period ending October 31st, 2023 (FY2023). FCI benefitted from solid revenue growth buoyed by higher interest rates and increased consumer demand. Meanwhile, SBTT’s modest revenue growth was offset by higher Non-Interest Expenses. What can investors expect from both entities in the months ahead? We discuss below.

FirstCaribbean International Bank Limited (FCI)

For the twelve months ended October 31, 2023 (FY 2023), FirstCaribbean International Bank Limited (FCI) reported an Earnings Per Share (EPS) of TT$1.12, 51.8% above the previous comparable period.

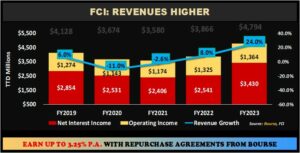

Notably, Total Revenue grew to TT$4.79B (FY 2023), up 24%, from the previous TT$3.87B (FY 2022). Operating Expenses expanded 9.7% to TT$2.78B, resulting in 51.2% improved performance of Total Net Revenue to TT$2.02B. FCI’s Credit loss expense on financial assets expanded from TT$67.9M (FY2022) to TT$74.9M (FY2023), owing to less favourable forward-looking economic indicators and a lower provision for credit losses. Income Before Tax (PBT) amounted to TT$1.94B, 53.4% higher than the prior period. Although FCI’s Tax Expense of TT$194.4M, grew 26.0% year-on-year, the Group’s effective tax rate dropped to 10.0% from a previous 12.2%. When compared to the previous comparable period, Net Income for the period climbed to TT$1.81B from the previous TT$1.18B, up 53%, resulting in overall Net Income Attributable to Equity Holders amounting to TT$1.77B, relative to TT$1.16B in the prior period, representing a 52.6% increase to shareholders.

Revenue Climb

Total Revenue improved sharply, growing at a faster rate from 8% (FY2022) to 24% Year on Year (YOY). According to FCI, the increase in revenue was caused by the normalization of transaction-based operating income within the region, as well as continued increases in US benchmark interest rates. Net Interest Income, the Group’s primary revenue source (71.6%), increased 35% to TT$3.43B, yielding improved results in its Bahamas and Cayman operations. The Group’s loan portfolio was relatively flat, declining by a modest 0.24% from TT$44.6B in FY 2022 to TT$44.4B in FY 2023. Operating Income (accounting for 28.4% of Total Revenue) expanded marginally by 2.9%, owing to higher transaction volumes.

Operating Segments Mixed

FCI’s Profit Before Tax (PBT) grew to TT$1.94B in FY 2023 compared to TT$1.27B in the prior comparable period, improving at an annualized rate of 53.4%. The Bank’s largest contributor to PBT growth, Corporate and Investment Banking (85.6% of PBT), advanced 52.4% from TT$1.09B to TT$1.66B, likely due to higher income on performing loans. Personal & Business Banking (PBB) contributed 7.7% to PBT, producing a 72.0% improvement year on year from TT$87M relative to TT$149M. The Wealth Management (WM) segment (3.7% of PBT) lowered from TT$74M in FY2022 compared to TT$71M in FY 2023, representing a decline of 2.8% in the current period.

The Bourse View

FCI currently trades at a price of $7.00 at a trailing P/E ratio of 6.2 times, below the Banking Sector average of 14.6 times. The stock offers investors a trailing dividend yield of 4.8%, above the sector average of 3.6%. The Group announced an interim dividend of US$0.0125 (TT$0.08) per share payable to shareholders on January 18, 2024. Recently, the Group disclosed the results of the last two divestitures which aligns with the company’s strategic objectives to streamline operations throughout the region, this included the sale of the Group’s assets in Curacao and St. Maarten to Curacao-based OrCo Bank N.V., and completion is anticipated during the first half of fiscal year 2024. Also noteworthy, FCI recently reported that it will be changing its legal name to CIBC Caribbean Limited which will align with the adoption of the CIBC brand, subject to regulatory approval. Projected lower benchmark USD rates in 2024, could weigh on FCI’s Net Interest Income generation moving into FY2024, though the timing and magnitude of lower rates remain relatively uncertain. On the basis of relatively increased revenue growth, attractive P/E multiples and USD dividends, Bourse maintains an OVERWEIGHT rating on FCI.

Scotiabank Trinidad and Tobago Limited (SBTT)

Scotiabank Trinidad and Tobago Limited (SBTT) reported Earnings per Share (EPS) of $3.85 for the full year period ended October 31st, 2023 (FY2023), a 0.8% decrease compared to $3.88 in the prior comparable period.

Net Interest Income improved 13.5% to $1.4B, while Other Income fell 19.7% from $651.8M in FY2022 to $523.1M in FY2023. Overall, Total Revenue for FY2023 came in at $1.9B, a 2.1% increase from the prior period. Non-Interest Expenses shifted 9.8% higher from $737.4M in FY2022 to $809.5M in FY2023, due to higher activity-related and technological costs. As a result, its operating efficiency ratio (expenses relative to revenue generation) increased from 38.9% to 41.8%. SBTT recorded a 3.8% reduction in Net Impairment Loss on Financial Assets, amounting to $105.9M (FY2022: $110.1M). Income before Taxation (PBT) stood at $1.0B, 2.7% lower relative to $1.1B recorded in FY2022. Income Tax Expense declined to 6.3% in the period under review, which led the taxation expense rate to decrease to 33.6% from 34.9% in FY2022. Overall, SBTT reported a Profit for the Period of $678.0M, down 0.8% compared to $683.7M in FY2022.

Revenue Higher

SBTT’s Total Revenue grew in FY2023 (up 2.1%). Net Interest Income, the Group’s largest revenue contributor (FY2023: 73.0%) rose by 13.5% to $1.4B, driven by continued credit expansion and decisive management of their investment portfolio. Meanwhile, Other Income (27.0% of Total Revenue) recorded a 19.7% declined, primarily due to lower trading revenues, aligned with prevailing market conditions.

The Bank’s largest operational segment by revenue, Retail Corporate & Commercial Banking (89.4% of Total Revenue) expanded 1.6% while its segment Asset Management contracted 20.6%, year-on-year. Its Insurance Services segment gained by 10.6% in FY2023, as they continue to leverage its customers’ existing banking relationships by offering their products.

Loans Increase, Impairment Expenses Fall

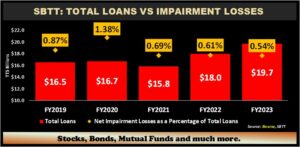

SBTT recorded a 9.6% increase in its Total Loan Portfolio from $18.0B in FY2022 to $19.7B in FY2023, indicative of favourable economic conditions and the Bank’s continued focus on meeting customers’ lending needs.

Loans to Customers (94.5% of Total Loans), the Bank’s largest interest-earning asset pool, expanded 7.5% to $18.6B, with contribution from all segments while simultaneously improving the credit quality of the portfolio. Loans and advances to banks and related companies advanced 67.1% year-on-year from $652.6M to $1.1B in FY2023. Net impairment losses on financial assets for the year were $105.9M, a decrease of $4.2M or 3.8% resulting in a decline in the ratio of Net Impairment Losses to Total Loans to 0.54% in FY2023 from 0.61% in FY2022, signalling an improvement performance of its loan portfolio.

The Bourse View

SBTT is currently priced at $69.98, 10.4% lower year-to-date. The stock trades at a Trailing Price to Earnings ratio of 18.2 times, above the Banking Sector average of 14.6 times and offers investors a Trailing Dividend Yield of 4.0%, higher than sector average of 3.6%.

SBTT declared a final dividend of $0.70, per share payable on January 19th, 2024, to shareholders on record by December 29th, 2023. Cumulatively, SBTT is paying a Total Dividend of $2.80 for FY2023, 15.2% lower than the $3.30 paid in FY2022. The bank’s commitment to robust dividend payments is evident in its 73% dividend pay-out ratio for FY2023, making it an appealing value proposition for income-oriented investors. On the basis of increased revenues, tempered by elevated valuations and higher non-interest expenses, Bourse maintains a MARKETWEIGHT rating on SBTT.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase, or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives, or agents, accepts any liability whatsoever for any direct, indirect, or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”