FCI HY2023

- Earnings: Earnings Per Share 69.8% higher, from TT$0.60 to TT$0.36

- Performance Drivers:

- Increased Revenues

- Higher Operating Expenses

- Outlook:

- Interest Rate Normalization

- Continued Economic Recovery

- Rating: Maintained at OVERWEIGHT

SBTT HY2023

- Earnings: Earnings Per Share 3.5% lower, from $2.02 to $1.95

- Performance Drivers:

- Higher Revenues

- Increased Expenses

- Outlook:

- Economic Normalization

Rating: Maintained at MARKETWEIGHT

This week, we at Bourse review the performance of Scotiabank Trinidad & Tobago (SBTT) and FirstCaribbean International Bank Limited (FCI) for their fiscal six-months (HY2023) period ended April 30, 2023. SBTT’s profitability was adversely impacted by higher expenses, while FCI benefited from increased revenue supported by improved economic activity. Could FCI continue to grow its earnings? Can SBTT effectively manage expenses as the financial year progresses? We discuss below.

FirstCaribbean International Bank Limited (FCI)

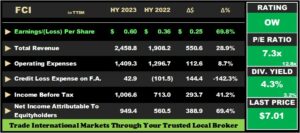

FirstCaribbean International Bank Limited (FCI) recorded Earnings per Share (EPS) of TT$0.60 for the six months ended 30th April 2023 (HY2023), up 69.8% compared to prior comparable period (HY2022).

Total Revenue expanded from TT$1.91B to TT$2.46B, an increase of 28.9%. Operating Expenses grew 8.7% year on year from TT$1.3M in HY2022 to TT$1.4M which – according to FCI- was primarily due to spending on strategic initiatives and higher employee-related costs. FCI reported a Credit Loss Expense on Financial Assets in the amount of TT$42.9M in HY2023 versus a reversal of TT$101.5M in the prior period. Income Before Tax (PBT) stood at TT$1.0B, 41.2% higher than TT$713.0M in HY2022. Resultantly, FCI reported an Income Tax Expense of TT$61.96M (46.6% lower). Overall, the Group reported Net Income Attributable to Equity Holders of TT$949.4M, up 69.4% from a prior TT$560.5M.

Operating Segments Improve

FCI’s PBT expanded 41.2% to TT$1.0B in HY2023 from TT$712.8M in HY2022, with growth reported across all operating segments.

FCI’s Corporate and Investment Banking (CIB) segment accounted for 85.2% of PBT and reported a Profit Before Tax of TT$837M, 20.2% higher YoY, owing to a reversal of Credit Loss Expense on Financial Assets of TT$54.5M in the period. Retail, Business and International Banking (RBB) recorded a Profit Before Tax of TT$107M in HY2023 advancing 218.9% compared to TT$33M in the prior comparable period, likely due to increase in card spending. Wealth Management recorded an increase in PBT from TT$21M to TT$38M, up 79.5% in HY2023, as segmental revenue grew 23.7%, attributable to favourable financial markets during the period.

Rationalizing Caribbean Footprint

FCI has continued a path to rationalize its operations and overall Caribbean footprint. On January 31st, 2023, the Bank ceased its operations in Dominica. On March 24th, 2023, FCI completed the sale of its banking assets in St. Vincent upon the satisfaction of the closing conditions. For the six months ended, April 30th, 2023, the associated net gain from the closure of Dominica and St. Vincent stood at TT$38M.

On May 18th. 2023 – the Bank wholly owned subsidiary, FCIB Barbados received regulatory approval to sell its banking assets in Grenada, with the transaction expected to close in July 2023.

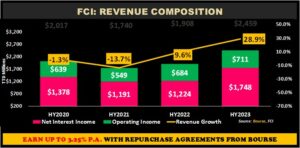

Higher revenues reflect rate environment

FCI’s Total Revenue advanced 28.9% to TT$2.4B in Q12023. Net Interest Income, the Group’s largest revenue contributor (Q12023: 83%) expanded 20.2% to TT$837M, supported by higher US interest rates in its US dollar denominated businesses, increased loan growth and improved regional economic activity. Loans and Advances to Customers expanded 8.5% year on year from TT$41.8B to TT$45.3B in HY2023. Operating Income, which includes net fees and commission income accounted for 28.9% of Revenue and expanded 3.9% to TT$106.1M.

The Bourse View

FCI trades at a current price of TT$7.01, up 28.6% year-to-date. The stock trades at a trailing 12-month P/E ratio of 7.3 times, significantly below the Banking sector’s average of 12.8 times. The stock also offers investors a Trailing Dividend Yield of 4.3%, above the sector average of 3.2%. The Group declared an interim dividend payment of TT$0.083 (US$0.0125) per share to be paid on July 7th, 2023.

FCI has benefitted from a recovery in economic activity across its tourism-based jurisdictions, as reflected by increased revenues. However, lingering inflationary pressures may continue to weigh on consumer habits in the near to medium term. On the basis of improved performance, relatively attractive valuations and US dollar dividends, Bourse maintains an OVERWEIGHT rating on FCI.

Scotiabank Trinidad and Tobago Limited (SBTT)

Scotiabank Trinidad and Tobago Limited (SBTT) reported earnings per share (EPS) of $1.95 for the half year ended April 30th, 2023 (HY2023), a 3.5% decrease compared to $2.02 in the prior comparable period.

Net Interest Income rose 16.4% to $694.5M, while Other Income fell 21.4% from $356.0M in HY2022 to $279.6M in HY2023. Total Revenue for HY2023 came in at $974.2M, a 2.3% increase from the prior period. Non-Interest Expenses shifted 9.4% higher from $360.5M in HY2022 to $394.3M in HY2023, as a result of higher activity costs as a result of increased business activity levels and the impact of inflationary pressures in the global economy. SBTT recorded a 25.8% expansion in Net Impairment Loss on Financial Assets, amounting to $57.1M (HY2022: $45.4M). Income before Taxation (PBT) stood at $522.8M, lower relative to $546.5M recorded in HY2022. The Taxation expense rate moved to 34.2%, marginal change from 34.7% in the prior comparable period. Overall, SBTT reported a Profit for the Period of $344.0M, down 3.5% compared to $356.5M in HY2022.

Revenues Higher

SBTT’s Total Revenue ($694.5M for the period ended 30th April, 2023) recorded an increase of $25M or 2.3%. This was attributable to growth in Net Interest Income (71.3% of Total Revenue), which rose by $98M to $695M in HY2023. According to the Group, this increase was driven by higher loan volumes to retail and commercial customers combined with greater yields on the Group’s investment portfolio.

Other Income (287% of Total Revenue) recorded a decrease from $354M to $280M in the current period under review, representing a 21.0% decline, due to lower trading revenues.

From an operating segment perspective, revenue growth occurred across all segments. The Bank’s largest operational segment by revenue, Retail Corporate & Commercial Banking (90.3% of Total Revenue) expanded 2.0% year-on-year. The Asset management segment experienced an 8.8% increase from the prior comparable period. Its Insurance Services segment displayed growth of 4.5%.

Loans, Impairment Expenses increase.

SBTT recorded a 6.3% increase in its Total Loan Portfolio from $17.6B in HY 2022 to $18.7B in HY2023, as continued recovery in economic activity supported loan demand.

Loans to Customers (94.8% of Total Loans), the Bank’s largest interest earnings asset, saw an increase of $1.5B or 9.0% rise, driven by increased demand following competitive offerings made to both retail and commercial segments. Loans and advances to banks and related companies decreased 41.1%.

Net Impairment losses on financial assets were recorded at $57.0M for the current period under review (26% increase year over year), resulting in an increase in the ratio of Net Impairment Losses to Total Loans to 3.05% in HY2023 from 2.56% in HY2022. Future performance will be dependent on the Bank’s ability to expand its loan portfolio, while employing strategies to keep expenses in check.

The Bourse View

SBTT is currently priced at $76.17 and trades at a Trailing Price to Earnings ratio of 20.0 times, above the Banking Sector average of 12.8 times. The stock offers investors a healthy Trailing Dividend Yield of 4.5%, above the sector average of 3.2%. The Group declared an interim dividend payment of $0.70 per share to be paid on July 11th, 2023, 7.7% higher than the $0.65 paid in the prior comparable period.

SBTT’s resolute dividend payments remain an attractive value proposition to owning the stocks, reaffirming its commitment to rewarding shareholders with consistent cash flows. On the basis of improved performance and consistent dividend payments but tempered by elevated sector valuations and local and global inflationary concerns driving up expenses, Bourse maintains a MARKETWEIGHT rating on SBTT.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”