BOURSE SECURITIES LIMITED

20th January 2020

Will Bond markets repeat 2019 performance in the New Year?

This week, we at Bourse review the performance of both the local and international fixed income market for 2019 and consider the investor outlook for bonds in the year ahead.

Low yields, Excess Liquidity, Low inflation persist

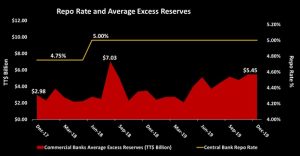

The Monetary Policy Committee (MPC) of the Central Bank of Trinidad and Tobago maintained its repo rate at 5.00% in December 2019, unchanged since September 2018. The MPC cited (i) “shifts in external conditions” as trade and geopolitical tensions soften, (ii) growth in the domestic energy sector with petrochemicals registering a year on year (y-o-y) increase of 23.3%, and (iii) the contraction of private sector and business credit 4.3% and 5.5% respectively while consumer credit grew 5.9% as reasons for the decision.

Excess Liquidity continues to grow in the financial system with Commercial Bank Excess Reserves up roughly 56% or TT$1.95B y-o-y. The substantial growth in excess liquidity, among other factors, contributed to generally low bond yields. The Trinidad and Tobago Treasury Yield Curve trended mostly lower with some buoyancy in the medium term. The most notable changes occurred at the 2-year yield, which declined 0.54% to 2.56% in December 2019 from 3.10% in December 2018, while the 15-year yield advanced 0.20% reaching 5.30% from 5.10% for the same period.

Headline Inflation- the rate at which prices increase- fell from 1.4% in January 2019 to 0.3% in November 2019. Inflation typically erode the real return- the return on an investment adjusted for inflation- for investors as rising cost of living wear away gains. This current reported low inflation environment would have enhanced the attractiveness of local bond markets, while also contributing to ‘depressed’ yields.

International Bond Markets Advance

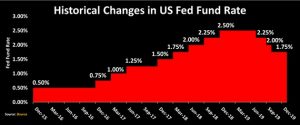

In an about-turn of events, the US Federal Reserve (Fed) cut interest rates by 25 basis points (bps) three times in 2019, instead of the two interest rate hikes initially anticipated. The US Fed cut US interest rates in July 2019, the first time since the Financial Crisis in 2008. The US Fed has since paused on increasing rates. The surprise cuts in rates throughout 2019 supported strong price advances and drops in yield across most international bond markets.

Emerging Market Bond Prices climb

Investors in Investment Grade (IG) and High Yield (HY) US dollar denominated Emerging Market (EM) bonds experienced positive returns to their portfolio for 2019. IG bonds provided total returns of around 14.0%, while HY bonds delivered 11.5% for 2019, as compared to the negative Total Returns of -1.1% and -4.7% for IG and HY bonds respectively for 2018.

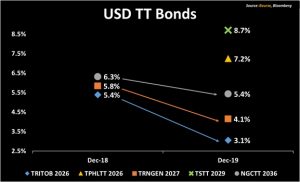

Trinidad and Tobago US dollar denominated bonds were no exception, despite a credit rating downgrade by S&P Global Rating (S&P) in July 2019 from BBB+ to BBB. The Government of the Republic of Trinidad and Tobago’s US dollar denominated bond due 2026 (TRITOB 2026) yield fell from 5.38% in December 2018 to 3.05% in December 2019, with a commensurate increase in market price. Local quasi-sovereign firms’ US dollar debt yields – including Trinidad Generation Unlimited’s bond due 2027 and the National Gas Company of Trinidad and Tobago’s bond due 2036 (NGCTT 2036) – fell as well from 5.8% and 6.3% in December 2018 to 4.1% and 5.4% in December 2019 respectively.

New issues of T&T US dollar bonds in 2019 included Trinidad Petroleum Holding Company Limited’s US$570 million bond due 2026 (TPHLTT 2026) in June 2019. This bond was utilized to partially repay the company’s outstanding debt due August 2019 and May 2022. The Telecommunication Services of Trinidad and Tobago also issued a new US$300 million aggregate principal bond due 2029 (TSTT 2029) in October of 2019. The bond, rated BB- by S&P and B2 by Moody’s, was oversubscribed, paying investors a coupon rate of 8.875% per annum.

In addition to lower US interest rates, greater clarity on geopolitical uncertainties such as the US-China trade war and Brexit bolstered investor confidence. While fears of a US recession briefly led to an inversion of the US Treasury Yield Curve, concerns waned toward the end of 2019.

Investing in 2020

Fixed income opportunities for investors with TT dollars were relatively few and far between in 2019. 2020, however, promises to bring more new opportunities to local bond investors. The Honourable Minister of Finance mentioned several new issues during the budget presentation in October 2019, including a second NIF bond, a TT$1 billion, 5-year Housing Bond at a rate of 4.5% and TT$3 billion in Government Vat Bonds at a rate of 1.5% for 5 years. The Tobago Hose of Assembly (THA) was also granted approval to raise financing utilizing bonds amounting to TT$300 million.

Internationally, the low interest rate environment is likely to persist into 2020, making investors’ search for returns more challenging. Investors seeking USD fixed income opportunities may wish to consider their investment horizon and risk tolerance in addition to examining the credit quality and liquidity of bond issues when investing. Investors should consult a trusted and experienced advisor, such as Bourse, to make better-informed decision.

For more information on these and other investment themes, please contact Bourse Securities Limited, at 226-8773 or email us at invest@boursefinancial.com.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”