Sagicor, JMMB Profits Decline

| HIGHLIGHTS

SFC 9M 2020

JMMBGL HY 2021

|

This week, we at Bourse review the financial performance of Toronto-listed Sagicor Financial Company Limited (SFC) for the nine-month period ended, September 30th 2020 and JMMB Group Limited (JMMBGL) for its fiscal half year ended September 30th 2020. SFC reported a loss on account of lower revenue growth, higher impairment losses and share of loss of associates. JMMBGL, which owns a 22.5% stake in SFC, recorded lower earnings on account of similar factors.

Sagicor Financial Company Limited (SFC)

For the nine-month period ended September 30th 2020 (9M 2020), SFC reported a Fully Diluted Loss Per Share of US$0.22, a 151.5% reversal from an EPS of $0.43 in the prior comparable period.

Net Premium Revenue, the Group’s core revenue driver closed the period at US$892.5M a 5.2% decline from US$941.1M reported in 9M 2019, impacted by a one-time single premium annuity in 9M 2019. Other Investment Income of US$84.0M shifted to an Expense of US$24.0M and Credit Impairment Losses increased to US$24.0M. Total Revenue fell 13.7% moving from a prior US$1.4B to US$1.2B. Total Benefits in the period declined 13.7% to US$766.7M. Meanwhile, Total Expenses in the period increased 1.0% to US$403.2M. SFC recorded a Share of Operating Loss of US$33.3M from a previous Share of Profit of US$8.8M. Income Before Tax swung from US$116.7M to a loss of US$0.7M in 9M 2020. Overall, Net Income for the Period declined 137.1% from US$79.5M in 9M 2019 to a Loss of US$29.5M in period under review. Net (Loss)/Income attributable to Equity holders stood at a loss of US$32.6M relative to a prior profit of $33.0M, 198.8% lower.

Operational Segments Decline

Net Income from Continuing Operations in SFC’s four main segments sharply declined from one period ago. With the COVID-19 pandemic upending business activities in the Group’s operating jurisdictions, only two of Sagicor’s four operational segments returned a positive bottom line.

Sagicor Jamaica generated a Net Income from Continuing Operations of US$42.6M, 53.3% lower than the prior period. Although reporting improvements in Net Premium Revenue, higher credit loss expenses and impairment losses from associate entity, Playa Hotels & Resorts weighed on the segment’s performance. SFC’s Share of Operating Loss of Associates and Joint Ventures of US$33.3M primarily stemmed from Sagicor Jamaica’s holding in Playa Hotels & Resorts. Sagicor Life reported a Net Income from Continuing Operations of US$12.9M, 58.0% lower than a preceding US$30.7M. A 179% (US$106.1M) increase in Net Benefit and a decline in topline growth were influencing factors for the decrease in profit.

Sagicor Life USA reported a Net Loss from Continuing Operations of US$35.9M due to a decline in the profitability of its investment portfolio and increased expenditure from upward revisions of Changes in Actuarial Liabilities relative to the prior year. Head Office and Other also contributed a Net Loss from Continuing Operations of US$49.2M as expenditure grew relative to a fall in income. Both these segments were responsible for SFC’s Net Loss in the period.

Operational Jurisdictions Weaker

Jamaica, SFC’s largest geographical segment by revenue (35.1%), declined 13.8% YoY from US$489.8M to US$422.2M. The USA accounted for the second largest share of Revenue generated by region, delivering $396.8M in 9M 2020, 17.8% lower than $482.6M in 9M 2019. Declines in market performance and disposable income ultimately weighed on revenue growth. Similarly, Trinidad and Tobago as well as Other Caribbean which collectively accounts for 20.7% of Revenue by geography experienced some challenges to top line growth. However, Barbados (11.3% of Revenue) has shown resilience in the current environment, improving 6.3%.

Buyback Optimism short-lived?

On the 4th of September, SFC received approval from the Toronto Stock Exchange to increase the its share buyback program to 8M common shares from 3M. As at the close of 9M 2020, 2.588M common shares were repurchased, suggesting share buybacks could continue. Results, however, appear to be overshadowing buyback-related optimism, with SFC’s share price correcting in recent days. Despite, the decline in its performance, SFC’s maintains a significant cash base at US$384.2M in 9M 2020, 40.7% higher YoY, which could potentially support its buyback program.

The Bourse View

Sagicor Financial Company Limited is currently priced at CAD$6.05 and trades at a market to book ratio 0.67 times relative to a peer average 0.96 times. The stock offers investors a trailing dividend yield of 4.9% in line with a peer average 4.9%. The Group declared a fourth quarter dividend of US$0.05625, payable on December 16th 2020. The Group’s ability to maintain consistent USD dividend payments could be tested should weaker performance persist, although the stabilization of financial markets will reduce the risk of dividend cuts. Despite its apparent deep value (evidenced by a steep market-to-book discount), with economic uncertainty still persisting in its key operating jurisdictions, Bourse maintains a NEUTRAL rating on SFC.

JMMB Group Limited (JMMBGL)

JMMBGL reported a 28.1% decline in its Earnings Per Share which amounted to TT$0.06 at the end of HY 2021 relative to TT$0.08 in HY 2020.

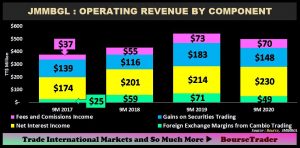

Net Interest Income rose 7.8% to TT$230.4M relative to a prior TT$213.7M. However, Income generated from the Group’s investment activities and services suffered a contraction, leading to 7.9% decline in JMMBGL’s Operating Revenue Net of Interest Expense. Operating Expenses amounted to TT$330.9M, a 3.3% decline from a previous TT$342.3M, illustrating some cost containment. Impairment Losses were up 26.1% in the period resulting in an expense of TT$17.2M compared to a previous TT$13.6M. Operating Profit decreased 18.7%, from TT$185.3M to TT$150.7M. Share of Loss of Associate standing at TT$4.94M, significantly influenced the year on year performance of JMMBGL. Profit Before Tax in HY 2021 was TT$145.8M, down 21.3% from TT$185.4M in HY 2020. Overall, Profit for the Period was TT$111.6M relative to TT$129.4M, 13.8% lower. Profit Attributable to Equity holders was TT$108.0M, 14.2% less than TT$125.9M in the prior comparable period.

Revenue Streams Broadly Lower

JMMBGL’s Net Interest Income grew 7.8% in the period as the Group reported a 33.8% expansion of its Loans and Notes Receivables portfolio. The year-on-year growth in the size of the Group’s loan portfolio comes despite the prevailing adverse economic conditions.

The impact of economic challenges was more evident in JMMBGL’s investment management and foreign exchange business lines. Revenue generated from Foreign Exchange Margins from Cambio Trading was 29.9% lower (TT$21.1M). Similarly, Fees and Commissions Income was down 4.5% or TT$3.3M. Declines in regional financial markets weighed on the revenue generation ability of Gains on Securities Trading, which contracted 19.1% in the period, TT$34.9M lower than prior year.

JMMBGL’s 7.9% reported decrease of Operational Revenue was attributable to decline in capital markets and relatively muted demand for Financial and Related Services. However, as regional economies embark on the path towards economic normalisation, there remains potential for recovery in the Group’s revenue generating ability.

Sagicor Records Loss

For the period ended HY 2021, JMMBGL reported a Share of Loss of Associate of TT$4.94M a further deterioration from $0.41M recorded in Q1 2021, attributable to a decline in the performance of SFC. At the close of the period, JMMBGL reported Interest in Associated Company at a value of TT$1.70B. With the market price of SFC at CAD$6.05, JMMBGL’s holding in SFC is currently valued at TT$1.06B, 37.6% less than the reported Carrying Value.

Preference Shares coming

On the 12th of November, JMMBGL issued notice of intention to conduct a public offering of Cumulative Redeemable Preference Shares, with offer and distribution solely occurring in Jamaica. Though details remain limited for now, proceeds could be potentially used to fund additional inorganic growth opportunities.

The Bourse View

JMMBGL is currently priced at $1.75 and trades at a trailing price-to-earnings (P/E) ratio of 10.7 times, just below the average of the Non-Banking Finance sector of 11.3 times. The stock offers a trailing dividend yield of 0.7%, below the sector average of 1.2%. JMMBGL declared an interim dividend payment of JMD$0.25 (TT$0.01), payable on December 31st 2020. JMMBGL could potentially benefit from financial market stabilization, with this outlook tempered by weaker credit conditions in its core operational regions of Jamaica, Trinidad and Tobago and Dominican Republic. On the basis of fair valuations, stabilizing financial markets but tempered by economic uncertainty and potential downward revaluations from JMMBGL’s equity stake in SFC Bourse maintains a NEUTRAL rating on JMMBGL.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”