BOURSE SECURITIES LIMITED

27th May, 2019

Alignvest-Sagicor deal progresses, NGL falls

This week, we at Bourse review the financial performance of Sagicor Financial Corporation (SFC) and Trinidad and Tobago NGL Limited (NGL) for their first quarters ended 31st March, 2019. While SFC’s earnings were weaker, progress on the Alignvest acquisition promises to provide additional value to Sagicor shareholders. Meanwhile, investors’ reactions to a possible shutdown of Atlantic LNG Company of Trinidad & Tobago’s (ALNG) Train 1 has sent the price of NGL shares lower over the past two weeks.

Sagicor Financial Corporation (SFC)

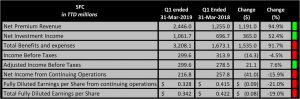

Sagicor Financial Corporation (SFC) reported total fully diluted Earnings per Share (EPS) from Continuing Operations of TT$0.33 for the first quarter (Q1) ended 31st March 2019, a 21.0% decline compared to TT$0.42 reported in Q1 2018.

SFC reported significant Revenue growth in Q1 2019. Net Premium Revenue almost doubled YoY, from TT$1.26B in Q1 2018 to TT$2.45B in Q1 2019. Net Investment and Other Income improved 52.4% or TT$365.0M, amounting to TT$1.06B for the period. Total Benefits and Expenses, however, increased 91.7% YoY, from TT$1.67B to TT$3.21B, in tandem with growth in Net Premium Revenue. SFC recorded a non-recurring gain of TT$35.4M in Q1 2018, arising from the acquisition of the British American Insurance Portfolio from the Government of Barbados. As a result, Income Before Taxes (PBT) amounted to TT$299.6M in Q1 2019, a 4.5% decline when compared to PBT of TT$313.9M in the prior comparable quarter. Adjusting for the one-off gain in Q1 2018, SFC’s PBT increased by TT$21.1M or 7.6% from the adjusted Q1 2018 PBT of TT$278.5M. Income Taxes were reported as TT$82.9M for the period, up 47.6% from TT$56.2M in Q1 2018. Overall, Net Income fell 15.9% YoY from TT$257.8M to TT$216.8M, attributable to the one-off gains recorded in 2018 as well as the consolidation of the Sagicor X Fund Group which contributed to the 11.4% increase in reported Expenses. According to the Chairman, excluding the consolidation effect, Expenses would have risen by a more moderate 4% YoY.

Outlook

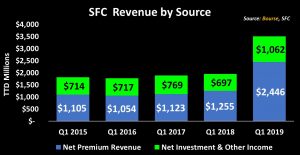

SFC’s Total Q1 Revenue has trended upward since 2016, with the most notable shift (+79.7%) occurring in Q1 2019. This was mainly attributable to a jump in Net Premium Revenue from TT$1.26B to TT$2.44B (+94.9%) stemming from significant expansion in SFC’s USA operations. The Group’s strategic decision to stop reinsurance of premiums to third parties, thereby retaining 100% of production would have also contributed to this net improvement. However, SFC would now have bear the full downside risk which would have previously been mitigated through reinsurance. Net Investment and Other Income also experienced YoY growth of 52.4% from TT$696.7 to TT$1.06B.

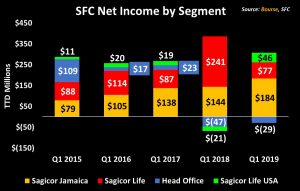

The performance of SFC’s various segments has generally varied year to year, with the exception of Sagicor Jamaica which has consistently reported improved first quarter Net Income since 2015 (Q1 2019: TT$183.8M; +27.7% YoY). The USA operations recovered from a Net Loss of TT$21.4M in Q1 2018 to an overall Net Profit of TT$46.2M in Q1 2019. Despite Revenue growth, the Sagicor Life segment recorded a 68.2% decline in Net Income, earning TT$76.7M for the Q1 2019 period.

Alignvest gets Shareholder Approval

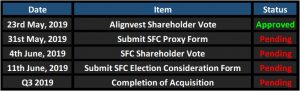

Alignvest (AQY) shareholders gave the green light on May 23rd, 2019 to the ‘acquisition’ of SFC, having received a majority (92%) shareholder approval and meeting the minimum cash requirement for the transaction. Of particular interest was the subscription agreement between AQY and JMMB Group Limited (JMMB), whereby JMMB would acquire a 20% shareholding in the new “Sagicor Financial Company Limited”. With the SFC Scheme of Arrangement Meeting fast approaching on 4th June, 2019, shareholders should be mindful of some important upcoming deadline dates. Proxy forms should be submitted by Friday 31st May, 2019 for shareholders on record as at 18th April 2019, while Election Consideration forms should be submitted by 11th June, 2019, following the Scheme meeting. These forms can be readily accessed either on the SFC website or at www.remotestores.com.

The Bourse View

At a current price of $9.20, SFC trades at a trailing P/E of 10.7 times, below the Non- Banking Finance sector average of 12.4 times (excluding NEL). The market-to-book ratio is 0.65, also below the sector average of 1.5. SFC offers investors a trailing dividend yield of 3.6%, above the Non-Banking Finance sector average of 3.0% (excluding NEL). On the basis of SFC’s attractive valuations, above average dividend yield and the expected upward growth trajectory upon successful completion of the Alignvest transaction, Bourse maintains a BUY rating on SFC.

Trinidad and Tobago NGL Limited (NGL)

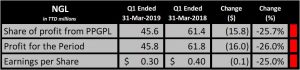

Trinidad and Tobago NGL Limited (NGL) reported Earnings per Share (EPS) of $0.30 for the first quarter (Q1) ended 31st March 2019, a 25% reduction from the EPS of $0.40 in Q1 2018.

The main driver of the downturn in NGL’s performance was a 25.7% reduction in the Share of Profit from Phoenix Park Gas Processors Limited (PPGPL), from $61.4M in Q1 2018 to $45.6M in Q1 2019. PPGPL derives its revenue from the processing of “wet” gas to NGLs and the fractionation of such NGLs to produce Propane, Butane and Natural Gasoline, which are then marketed and sold to domestic and international users. Average Mont Belvieu Prices of these commodities for Q1 2019 fell YoY by 19.5% 10.9% and 22.3% respectively. The effect on Revenue was tempered, however, due to 7.5% higher NGL sales volume YoY. Overall, Profit for the Period declined 26.0% from $61.8M to $45.8M.

BPTT announcement shakes investor confidence

Since its 2015 Initial Public Offering (IPO), most investors in TTNGL have become accustomed to the stock’s dividend stability, despite the cyclical nature of the energy industry. However, BP Trinidad & Tobago’s (BPTT) announcement that disappointing results from its drilling programmes could impact its forecast production in T&T (in particular for 2020 and 2021) has rattled shareholders of TTNGL. BPTT also noted that there could be “challenges” to its supply of gas to Atlantic LNG’s Train 1 after 2019.

Investors’ responses have been negative, with the price of NGL’s stock falling almost 14% from $30.09 on May 10, 2019 to $26.00 on May 24th 2019.

The big question: Is the market response to the news warranted, or is it an overreaction? A more detailed look at the impact of a possible shutdown of ALNG’s Train 1 on NGL’s fortune is available in an exclusive Research Note on the Bourse website, www.remotestores.com.

The Bourse View

At a current price of $26.00, NGL trades at a trailing P/E of 17.0 times, and remains one of the top five dividend paying stocks on the local exchange, offering investors a trailing dividend yield of 5.8%. NGL also maintained a healthy cash position of $2.86 per share as at 31st March, 2019. As explained in our Research Note (available at www.remotestores.com), several factors should be considered in assessing the potential impact of a Train 1 shutdown on NGL’s performance. Accordingly, Bourse maintains a BUY rating on NGL.

For more information on these and other investment themes, please contact Bourse Securities Limited, at 226-8773 or email us at invest@boursefinancial.com.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”