HIGHLIGHTS

AHL HY2023

- Earnings: Earnings Per Share increased 15.2% from $0.33 to $0.38

- Performance Drivers:

-

- Increased revenue

- Margin Improvements

- Higher Finance Costs

- Outlook:

- Increase sales in U.S. Market

- Rating: Upgraded to MARKETWEIGHT

WCO HY2023

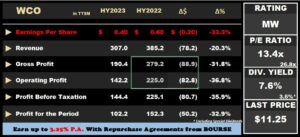

Earnings: Earnings Per Share decrease 33.3% from $0.60 to $0.40

- Earnings: Earnings Per Share decrease 33.3% from $0.60 to $0.40

- Performance Drivers:

- Reduced Revenues

- Lower Margins

- Outlook:

- New investments

- Rating: Maintained at MARKETWEIGHT

This week, we at Bourse review the performance of Angostura Holdings Limited (AHL) and The West Indian Tobacco Company Limited (WCO) for the six-month period ended 30th June 2023. AHL would have benefitted from increased revenue from both local and international markets, while WCO – despite a better quarterly performance – would have been constrained by reduced revenues and lower margins in the first half. How will both companies fare in the months ahead? We discuss below.

Angostura Holdings Limited (AHL)

For the six-month period ended June 30, 2023, Angostura Holdings Limited (AHL) reported Earnings per share (EPS) of $0.38, up 15.2% from the $0.33 earned in HY2022. Revenue climbed by 3.0% from a previous $460.0M in HY2022 to the current $473.8M. A 3.4% decrease in cost of sales contributed to gross profits increasing 9.3% from $232.9M to $254.5M. Selling and marketing expenses grew 8.8% to $93.2M, while administrative expenses also increased by 18.3% to $56.4M. Overall, AHL reported an increase in operating profits of 16.1%, from $89.5M in the previous comparable half year to $104.0M in HY2023. Inclusive of Net Finance Income, Profit Before Tax (PBT) for AHL increased from HY2022’s $98.4M to $111.8M, a 13.6% increase. Results showed a profit for the period of $77.8M for AHL, up 15.0% from the profit of $67.6M stated for the prior comparable period.

Revenue Higher

The Group’s local and global strategies and brand management were credited as helping AHL to improve revenue over the most recent comparable periods. Total Revenue for the most recent six-month period increased by 3.0%, from $460M in HY 2022 to $474M in HY 2023. Importantly, Revenue for AHL over the last four (4) Half-Year periods would have experienced consecutive increases. This trend of revenue growth would be encouraging for investors, with eventually moderating supply chain issues supporting improved margins in future. AHL did, however, allude to logistical and freight difficulties having an adverse impact on some international marketplaces.

Margins Trend Upward

AHL’s profitability margins all improved over the six-month reporting period. AHL’s Gross Profit margin showed notable improvement from 50.6% to 53.7%, driven by revenue growth and seemingly moderating input costs.

Operating Profit margin grew from 19.5% in HY2022 to 21.9%, while Profit After Tax margin expanded to 16.4% in HY2023 from 14.7% (HY2022). According to the company, profitability margins would have improved on account of production efficiencies and cost management strategies, along with the maintenance of a low debt ratio. The improvement in margins, like AHL’s revenue trends, have persisted over the past 4 comparable reporting periods.

The Bourse View

Angostura Holdings Limited (AHL) is currently priced at $22.55, down 6.0% year-to-date. The stock trades at a trailing P/E of 29.7 times, above the Manufacturing Sector average of 26.8 times. The group declared an interim dividend payment of $0.10 per share, to be paid to shareholders on September 29, 2023. The stock offers investors a trailing dividend yield of 1.6%, below the sector average of 3.6%.

Domestically, the Group is expected to benefit from seasonality factors in the fourth fiscal quarter, while international growth remains an area of focus and opportunity. Notwithstanding positive and persistent trends in revenue and margins, AHL trades at a relatively lofty Price-to-Earnings (P/E) ratio. This suggests that earnings may have to play ‘catch up’ with AHL’s stock price to justify its current level. This may make AHL better suited for investors focused on long-term growth of the company’s earnings, while placing less importance on cash flows in the form of dividends. On the basis of increased revenue growth and margins improvement but tempered by relatively high valuations, Bourse upgrades its rating on AHL to MARKETWEIGHT.

The West Indian Tobacco Company Limited (WCO)

The West Indian Tobacco Company Limited (WCO) reported Earnings Per Share of $0.40 for the six months ended June 30th, 2023 (HY 2023), a 33.3% decline from $0.60 reported in the prior comparable period.

Revenue fell 20.3% Year on Year (YoY) from $385.2M to $307.0M, accompanied by an 11.1% increase in Cost of Sales. Consequently, Gross Profit fell to $190.4M, 31.8% lower compared to $279.2M reported in HY 2022. Increases in distribution costs of 28.7% and administrative expenses up 4.1%, offset the decline in other operating expenses, leading to an overall 36.8% drop in operating profit. Operating Profit contracted from $225.0M in HY 2022 to $142.2M in HY 2023. Profit Before Tax declined 35.9% to $144.4M due to an increase in finance income. Overall, WCO reported a Profit for the Period of $102.2M, down 32.9% from $152.3M reported in HY 2022.

2nd Quarter Signaling Stabilization?

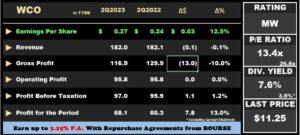

Notwithstanding the lacklustre six months (6M) performance (January-June), WCO’s 2nd quarter (April-June) 2Q2023 performance provided some cause for optimism when compared to the prior comparable period (2Q2022). Earnings Per Share came in at $0.27 for the three-months quarter ended June 30th,2023 (2Q2023), a 12.5% increase from $0.24 in prior comparable period (2Q2022).

Revenue was relatively flat at $182.0M in the quarter, while profits for the period were $68.1M, a 13% increase over 2Q2022. While not necessarily marking an end to WCO’s market challenges, 2Q2023’s performance could be an indicator of some degree of stabilization to company performance. Investors would understandably still be cautious, looking for additional data in subsequent quarters to support the stabilization/recovery narrative.

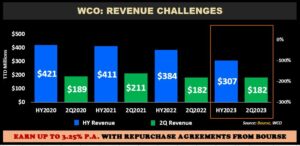

Revenue Lower

WCO’s revenue for its calendar first half (HY) continued to trend downward, declining 20.3% over the prior comparable period from $384M in HY2022 to $307M in HY2023. However, for the three months quarter two period, 2Q2022 reported revenue of $182.1M, and $182.0M for 2Q2023 representing a decline of only 0.1%. The company’s revenue was negatively impacted as consumers purchasing patterns changed, characterized by lower demand and an increasing appetite for lower-priced products. According to WCO, the company has observed positive returns in new recent investments which will accrue in quarters to come.

Margins Pressured

WCO’s Gross Profit Margin fell from 72.7% to 62.0% in HY 2023, following a 11.1% ($11.6M) increase in Cost of Sales likely owing to a combination of factors including increased costs of direct materials as stated in the previous quarter. Operating Margins fell to 46.3% in HY2023 relative to a prior 58.6%. Profit After Tax Margin deteriorated to 33.3% from 39.7% in the prior comparable period.

For WCO’s second quarter (April – June) 2Q2023, operating profit margins remained unchanged at 52.6% in 2Q2023. Its profit after tax margin improved notably to 37.4% in 2Q2023 from 33.1% in the prior comparable quarter.

The Bourse View

At a current price $11.25, WCO trades at a P/E of 13.4 times, well below the Manufacturing Sector average of 26.8 times. The company announced an interim dividend of $0.26 to be paid on August 29th, 2023, to shareholders on record by August 10th, 2023. The stock offers investors a trailing dividend yield of 7.6%, above the sector average of 6.9%. Excluding UCL’s abnormal and likely one-off dividend, the sector average dividend yield would stand at 3.6%.

WCO efforts to adapt to changing consumer preferences with investments in new business ventures and a focus on distribution is likely to take time to influence performance. On the basis of relatively attractive valuations, improved quarter-on-comparable-quarter profitability but tempered by revenue and margin pressures, Bourse maintains a MARKETWEIGHT rating on WCO.

DISCLAIMER: “This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase, or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives, or agents, accepts any liability whatsoever for any direct, indirect, or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”