TTNGL Earnings Drop as Energy Prices Languish

| HIGHLIGHTS

TTNGL HY 2020 · Earnings: EPS 80.9% lower, from $0.47 to $0.09. · Performance Drivers: o Lowered Demand for NGLs o Lowered Prices for NGLS and consequent decline in PPGPL’s earnings · Outlook: o Stabilizing but muted NGL prices o Longer-term growth through acquisitions · Rating: Maintained at NEUTRAL. Energy Markets · Year to Date Performance: o WTI Crude ↓ 38.6% o Brent Crude ↓39.5% o Henry Hub Natural Gas ↑2.7% · Outlook: o Potential continuation of muted prices in the short term o Gradually improvements to demand for energy commodities amid continuous steps toward normalization |

This week, we at Bourse review the performance of the Trinidad and Tobago NGL Limited (TTNGL) for the six-month period ended the 30th of June, 2020. TTNGL declined on account of lower Natural Gas Liquids (NGL) production and prices encountered by its solitary investee company, Phoenix Park Gas Processors Limited (PPGPL). After a challenging first half of 2020 for energy markets, energy commodity prices have stabilized to some degree. What does that imply for TTNGL? How important will energy markets be to T&T as it heads toward the FY2020/2021 budget? We discuss below.

Trinidad and Tobago NGL Limited (TTNGL)

TTNGL reported an Earnings Per Share (EPS) of $0.09 for the half year ended 30th June 2020 (HY 2020), an 80.9% decline from $0.47 reported in the prior comparable period. TTNGL received a Share of Profit from Investment in Joint Venture of $14.9M, 79.8% lower than a previous $73.8M, attributable to depressed natural gas liquids prices which impacted the performance of underlying holding, PPGPL. Total Income contracted by 79.7% to $15.2M from $74.8M. Overall, Profit for the Period amounted to $14.5M, an 80.2% decline from $73.4M in HY 2019.

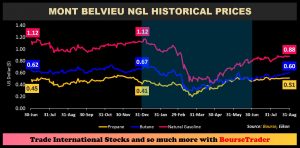

NGL Prices Stabilize

Natural Gasoline, which accounts for 47% of PPGPL’s exports, depreciated 42% Year-on-Year (YoY). The price of Butane (25% of exports) retreated 24% YoY whilst the price of Propane (28% of exports) declined 5%, showing relatively less volatility as compared to the other NGL.

Energy markets have recorded some improvement, with Propane recovering 130.0% to US$0.46/gallon from a historic low of US$0.20/gallon in March and Butane rebounding 78.7% from a low of US$0.29, also in March. Natural Gasoline prices, meanwhile, improved 85.7% from a low of US$0.43/gallon in April. As at the 11th of September, Propane was up 9.4%, while Butane and Natural Gasoline remained muted, down 11.5% and 27.5%, respectively.

Production Declines

Disruptions to energy markets caused by the COVID-19 pandemic and other factors contributed to a 6.5% YoY contraction in Natural Gas production. NGL production was also affected, falling significantly in HY 2020 to 4.0M barrels (BBLS) from 4.4M BBLS in the prior period. Comparatively, between HY 2016 to HY 2019 production fell at a rate of 0.1 BBLS per year. Exports reached its lowest level of 3.8M BBLS in HY 2020 from 4.5M BBLS in HY 2019 (15.3% lower).

An equally-weighted basket of NGL prices recorded a 34.8% YoY price decrease, to an average of $0.54 per gallon in the first half of 2020, from $0.83 per gallon in HY 2019 reflecting shifts in the energy sector due to economic conditions.

Outlook

In HY 2020, PPGPL benefitted from a 6% improvement in NGL content in gas streams. In addition to higher content gas streams accessed in 2020, PPGPL also stated its commitment to conservative cash management, intended to preserve its financial profile during more challenging periods as is currently the case.

The acquisition of Twin Eagle Liquids Marketing LLC, intended to build PPGPL’s profitability, is unlikely to materialize in the near-term with energy prices and trading muted. Investors may have to practice patience to reap the rewards PPGPL’s latest foray into asset diversification.

The Bourse View

At a current price of $16.14 (32.6% lower YTD), TTNGL trades at a trailing P/E ratio of 35.1 times. The stock also offers investors a trailing dividend yield of 1.6%. No mention of an interim dividend was made in the TTNGL’s financial release, consistent with its language of conservative cash management and in similar fashion to many other publicly listed companies which have greatly reduced or eliminated dividend payments under the prevailing uncertainty. With economic recovery hinged on the development of a COVID-19 vaccine, the timeline for an energy market recovery remains uncertain. On the basis of stabilizing energy prices, but tempered by less dividend certainty, muted economic activity and volatile Natural Gas processing volumes, Bourse maintains a NEUTRAL rating on TTNGL.

Oil Prices Lower but Stable

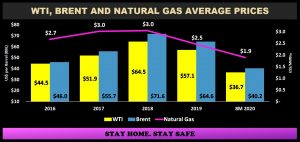

After encountering significant headwinds in early 2020, oil prices have in recent months recorded some recovery. Brent oil traded at an average price of $45.03 in August, while WTI traded at an average of US$42.39, both up from multiyear lows of US$19.33 and –US$37.63 respectively, in April. However, as at the 11th of September, prices remain muted with WTI down 38.6% and Brent down 39.5%. Natural Gas, however, has proven more resilient, with the commodity’s price advancing 2.7%, as at the 11th of September and averaging US$2.34/mmbtu in August.

For the first eight months of 2020, WTI has averaged US$36.66 per barrel while Brent has averaged a price of US$40.22 per barrel, these levels being 17.6% and 12.5% less than those recorded during the 2016 oil slump. Natural Gas meanwhile, has reported a 29.3% decline from 2016 levels and a 0.2% decline from the prior year average.

The ongoing research for a COVID-19 vaccine and the gradual easing of travel and trade restrictions have fuelled gradual improvement for the major non-renewable energy commodities.

Energy Prices Forecast to Stabilize

In its Short Term Energy Outlook published on the 9th of September, the US Energy Information Administration (EIA) raised its 2020 forecasts for WTI Crude 1.3% to US$38.99 per barrel and Brent, up 1.2% to US$41.90 per barrel. In the coming year, Brent Crude Oil is projected to average US$49.07 per barrel, while WTI Crude Oil is estimated to average US$45.07 per barrel.

Meanwhile, the Natural Gas price forecast was lifted 5.8% to an estimated price of US$2.49 per MMBtu in 2020. In 2021, the commodity price is projected to average US$3.19 per MMBtu.

Petrochemicals Prices Flounder

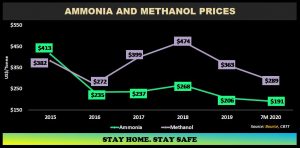

Further downstream, Ammonia prices have fallen in the last five years. In the 2015, the average price of Ammonia was US$413 per tonne, comparatively in 2019 it was US$206, eventually falling to an average of US$191 per tonne in the first seven months of 2020. The decline in Ammonia prices have influenced the profitability of domestic plants, including the permanent closure of one of Yara’s plants. Two additional plants (Nutrien PCS 02 and PCS 01) were temporarily closed in response to market prices.

The price of Methanol has shown more resilience in prior periods. In 2015, Methanol prices averaged US$382 per tonne, climbing as high as US$474 in 2018. 2019 prices fell to an average US$363 per tonne, falling again in the first seven months 2020, to an average price of US$289/tonne. In reaction to the downward shift in prices three Methanol plants (Titan, TTMC II and CMC) have taken the decision to indefinitely idle their operations.

Local Energy Prices Recovering

The Energy Commodity Price Index (ECPI) is a measure of average energy prices faced by domestic producers, based on T&T’s top ten energy commodity exports. The Index, which reflects international energy market conditions, fell to a historic low of 41.6 in April, eventually increasing to 59.9, most recently in July. Excess supply and lower demand of energy and energy commodities significantly affected energy prices in early 2020. However, with suppliers reactively cutting production and economies cautiously reopening, demand as well as market prices have relatively improved.

Investor Considerations

Trinidad and Tobago, primarily reliant on its export of energy based commodities, is likely to face lingering economic consequences due to the decline in energy prices. With lower prices and currently muted demand, reduced energy revenue and related foreign currency inflows into the economy is likely. The ripple effect of subdued energy revenues on the non-energy sector could also be significant, with both private and public sector spending likely to be adversely impacted.

Next week, we begin our 3-part series focused on the upcoming FY2020/2021 budget for Trinidad & Tobago, to be delivered on Monday October 5th.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”