HIGHLIGHTS

SBTT 9M2025

- Earnings: Earnings Per Share 8.7% higher, from $2.77 to $3.01

- Performance Drivers:

- Strong Revenue Growth

- Higher Non-Interest Expenses

- Outlook:

- Increased Economic Activity

- Rating: Maintained at MARKETWEIGHT

CIBC 9M2025

- Earnings: Earnings Per Share down 48.1% from TT$0.90 to TT$0.47

- Performance Drivers:

- Revenues Lower

- Higher Provision for Credit Losses

- Outlook:

- Increased Economic Activity

- Lower US Benchmark Interest Rates

- Rating: Maintained at MARKETWEIGHT

This week we at Bourse review the performance of locally listed Canadian banking giants, Scotiabank Trinidad and Tobago Limited (SBTT) and CIBC Caribbean Bank Limited (CIBC) for their respective nine-months reporting periods ended July 31st, 2025 (9M2025). SBTT’s performance was supported by improved revenue growth, while CIBC’s results were impacted by higher provision for credit losses. We discuss below.

Scotiabank Trinidad and Tobago Limited (SBTT)

Scotiabank Trinidad and Tobago Limited (SBTT) reported Earnings per Share (EPS) of $3.01 for the nine-month period ending July 2025, advancing 8.7% from $2.77 in the prior comparable period.

SBTT’s Net Interest Income grew by 8.8% to $1.15B. Other Income increased by 7.0% from $381.8M to $408.6M in 9M2025. Total Revenue for the period reached $1.6B, marking a 8.3% year-on-year increase. Non-Interest Expenses climbed 4.2% to $645.7M in 9M2025. SBTT reported a significant increase of 41.1% in Net Impairment Loss on Financial Assets, totaling $96.0M compared to $68.0M in 9M2024. Profit before Taxation rose by 8.8% to $819.0M, up from $752.7M in the last reporting period. Income Tax Expense increased to $288.0M (+9.0%), with an effective taxation rate of 35.2%. Overall, SBTT reported a Profit Attributable to Equity Holders of $531.0M, up 8.7% compared to $488.4M in 9M2024.

Increased Revenue

Net Interest Income, the Group’s largest revenue contributor (9M2025: 73.8%) rose by 8.8% year on year to $1.15B, driven by higher loan volumes across both the retail and commercial segments.

Other Income (26.2% of Total Revenue) amounted to $409M in 9M2025 (+7.0%), reflecting growth in core business operations across all segments.

From an operating segment perspective, revenue growth was reported across all segments. The Bank’s largest operational segment by revenue, Retail Corporate & Commercial Banking (91.0% of Total Revenue) rose 7.5% year-on-year. Its Insurance Services segment and the Asset Management segment both displayed growth of 20.7% and 2.9%, respectively.

SBTT’s efficiency ratio improved to 41.4% in 9M2025 from 43.0%, signaling enhanced operational efficiency. Non-interest expenses rose by $25.8M to $645.7M (+4.2%) in 9M2025, driven by inflationary effects alongside increased operating activity, as noted by the Group. Looking ahead, effective cost management will be key to sustaining profitability.

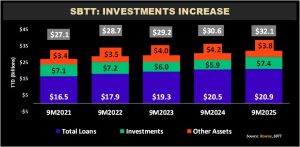

SBTT’s Total Assets climbed 4.8% year-on-year, increasing from $30.6B in 9M2024 to $32.4B in 9M2025, driven by a $1.0B increase in customer deposits, which provided funding for asset expansion.

Total Loans (65.2% of Total Assets) modestly increased 1.7% from $20.5B to $20.9B in 9M2025, reflecting consistent growth across the past five (5) year reporting periods. The Investment portfolio (Securities and Treasury Bills) totaled $7.4B, advancing 25.8% compared to the prior period, as the Group strategically deployed excess liquidity into investments.

The Bourse View

SBTT is currently priced at $48.50, down 15.3% year-to-date and trades at a Trailing Price-to-Earnings ratio of 12.2 times, above the Banking Sector average of 9.4 times. The stock offers investors a healthy Trailing Dividend Yield of 5.8%, above the sector average of 5.0%. The Group declared an interim quarterly dividend payment of $0.70 per share (Prior comparable period: $0.70/share) to be paid to shareholders on October 10th, 2025.

SBTT’s consistent dividend payouts remain an attractive option for income-focused investors, despite the presence of other banking sector stocks offering comparable or even higher dividend yields. On the basis of improved performance and consistent dividend payments but tempered by above average sector valuations, Bourse maintains a MARKETWEIGHT rating on SBTT.

CIBC Caribbean Bank Limited (CIBC)

For the nine-months ended July 31st, 2025(9M2025) CIBC Caribbean Bank Limited (CIBC) reported an Earnings Per Share (EPS) of TT$0.47, a 48.1% reduction from the TT$0.90 recorded in 9M2025.

Total Revenue came in at TT$3.5B, down 7.4% from the previous TT$3.7B in 9M2024. Operating Expenses increased by $159M to TT$2.3B, mainly driven by reported higher non-credit losses, investment in key strategic initiatives as well as engagement in Corporate Social Responsibility. Credit loss expense on financial assets increased 1307%, from TT$234.3M in 9M2025 compared to TT$17.9M in 9M2024. Income Before Tax (PBT) fell to TT$892.0M, a 42.3% decline from TT$1.5B in the previous period. CIBC’s Income Tax Expense jumped 29.9% to TT$144.9M from TT$111.6M, due to the company’s transition to the global minimum corporate tax framework. As a result, Net Income for the period dropped by 47.3% to TT$766.8M, compared to TT$1.02B in 9M2024. According to the Group, after excluding the fair value loss which consists of structured notes issues by a third-party fund, Adjusted Net Income stood at TT$1.1B, down 24.7% from an adjusted TT$1.5B in the prior period. Overall, Net Income Attributable to Equity Holders declined by 48.0%, from TT$1.4B in 9M2024 to TT$739.7B in 9M2025.

Revenue Lower

Total Revenue experienced a 7.4% year-on-year (YoY) decline, moving from TT$3.7B in 9M2024 to TT$3.5B in 9M2025. Net Interest Income, which represents 77.9% of Total Revenue, improved 0.5% to TT$1.8B from TT$1.9B a year earlier. Impressively, the bank’s loan portfolio continues to advance, improving by TT$2.6B to TT$48.0B in 9M2025. Operating Income (accounting for 22.1% of Total Revenue) moved from TT$1.1B (9M2024) to TT$767M in 9M2025, a 27.6% decline. According to the Company, overall revenue performance was impacted by softer US interest rates, higher funding costs, along with a loss on non-core investment in structured notes issued by a third-party.

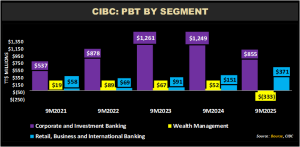

PBT by Segment

CIBC’s Profit Before Tax (PBT) dropped by 42.3% Year over Year (YoY), driven by lower revenue across most segments. The Bank’s largest contributor to PBT Corporate and Investment Banking (95.9% of PBT), decreased 31.6% from TT$1.2B to TT$855M. However, Retail, Business and International Banking (PBB) experienced significant growth, improving 145.4% to TT$371M in 9M2025. The Wealth Management (WM) segment faced significant pressures, sharply declining 736.7% YoY, moving from a Profit Before Tax of TT$52M to a Loss Before Tax of TT$333M.

The Bourse View

CIBC currently trades at a price of $8.25, up 1.9% Year to Date and at a trailing P/E ratio of 11.5 times, above the Banking Sector average of 9.4 times. The stock offers investors a trailing dividend yield of 4.1%, below the sector average of 5.0%. The Group announced an interim dividend of US$0.0125 (TT$0.08) per share payable on October 16th, 2025, to shareholders on record as of September 18th, 2025. Importantly, dividend payments are made to shareholders in US Dollars.

The U.S Federal Reserve’s decision to cut benchmark interest rates in September 2025, coupled with anticipated further reductions, is expected to place additional pressure on top-line performance. Nonetheless, continued growth in loan volumes may partially offset this impact.

On the basis of marginally higher interest income and USD dividends, tempered by reduced revenue and higher operating expenses, Bourse maintains a MARKETWEIGHT rating on CIBC.

This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”