HIGHLIGHTS

AMCL 9M2024

- Earnings: Earnings Per Share of $2.01, 23.3% higher than $1.63 in 9M2023

- Performance Drivers

- Modest Revenues

- Improved Margins

- Acquisition Activity

- Rating: Maintained as MARKETWEIGHT

GKC 9M2024

- Earnings: Earnings Per Share of TT$0.28 up 11.2% from TT$0.25 in 9M2023

- Performance Drivers:

-

- Revenue Growth

- Improving Margins

- Rating: Maintained at OVERWEIGHT

This week we at Bourse review the performance of two stalwarts of the Conglomerate sector on the Trinidad & Tobago Stock Exchange (TTSE), Ansa McAL Limited (AMCL) and GraceKennedy Limited (GKC) for their respective nine-month periods ended September 30th, 2024. AMCL and GKC both benefitted from improved revenues and profitability margins. Can both groups maintain this positive momentum in the upcoming periods? We discuss below.

Ansa McAL Limited (AMCL)

Ansa McAL Limited (AMCL) reported Diluted Earnings per Share (EPS) of $2.01 for the nine months ended September 30th, 2024 (9M2024), compared to an EPS of $1.63 reported in 9M2023.

Revenue amounted to $5.2B for 9M2024, up 2.1% or $108.9M year-on-year. Operating Profit improved 16.9% from $493.8M in 9M2023 to $577.1M in 9M2024. Finance costs dipped 21.0% to $29.1M. Share of Results from Associates and Joint Venture Interests advanced 77.2% to $20.2M (9M2023: $11.4M). Profit Before Tax increased 21.3% from $468.3M in 9M20223 to $568.1M in 9M2024. Taxation expense amounted to $159.1M in the current period under review, relative to $144.5M in 9M2023. The Group’s effective rate moved from 30.9% in 9M2023 to 28.0% in 9M2024. Profit for the Period rose to $409.0M, 26.3% higher than the $323.8 reported in the prior comparable period. Overall, Profit Attributable to Equity Holders climbed 23.5% to $347.4M.

AMCL reported Profit Before Tax (PBT) of $568M in 9M2024 relative to $468M in 9M2023. Its top-earnings segment (62.9% of PBT), Construction, Manufacturing, Packaging & Brewing, grew 33.9% YoY from $267M to $358M, increasing both in terms of revenue and profitability. Banking and Insurance services (26.2% of PBT) advanced 17.2% to $149M from $127M in prior comparable period. The Automotive, Trading & Distribution segment’s PBT contracted 5.0% to $125M, despite modest revenue growth. The Media, Services, Retail and Parent Company segment logged a loss of $63M, wider than the $57M loss recorded in 9M2023.

‘2X’ On Track

AMCL reinforced its commitment on its long-term growth strategy and its ambitious “2X” target for 2027 by continuing to pursue inorganic growth opportunities through acquisitions and/partnerships. Its most recent initiative is the acquisition of the US-based chlor-alkali producer, BleachTech LLC, via its US subsidiary, ANSA Chemicals Limited.

The Group purchased the Cleveland, Ohio based company at a price of US$327M, representing the largest acquisition in AMCL’s history. The transaction was closed on November 1st, 2024.

According to the Group, the acquisition is expected to improve AMCL’s Construction, Manufacturing, Packaging and Brewing segment and is expected to be materially accretive to earnings for its first full year of operations in 2025. According to Chief Financial Officer (CFO), Nicholas Jackman at its Broker Meeting on 11th November 2024 – BleachTech is set to contribute 8-9% of ANSA’s revenue. The Group also estimates that the acquisition’s contribution to Earnings per Share (EPS) could be in the vicinity of $1.00. Importantly, AMCL’s newly acquired asset does have significant capacity utilization prospects, currently operating at a reported 50% of rated output.

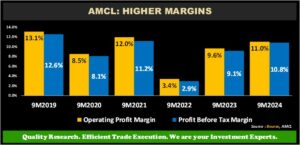

Margins Improved

AMCL’s profitability margins increased year-on-year but remained below the pre-COVID levels seen in 9M2019. In the first nine months of 2024, the Operating Profit Margin for AMCL stood at 11.0%, up from 9.6% in 9M2023. Profit Before Tax Margin in 9M2024 improved to 10.8%, up from 9.1% in 9M2023. AMCL’s BleachTech acquisition are likely to influence its margins in subsequent periods, though it remains unclear as to the particular direction at this time.

The Bourse View

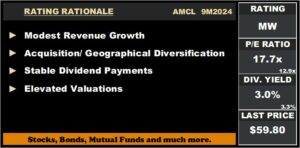

At a current market price of $59.80, up 10.6% year-to-date, AMCL trades at a trailing P/E of 17.7 times, above the Conglomerate sector average of 12.9 times. The stock offers investors a trailing dividend yield of 3.0%, below the sector average of 3.3%. The Group’s recent acquisition, if delivering returns as estimated, could prove to be impactful to valuations and creates a tangibly positive outlook on AMCL stock.

AMCL’s continues to enhance and add value to its existing operations via strategic partnerships and acquisitions, while concurrently diversifying its presence regionally and internationally. On the basis of increased revenue growth, continued acquisition activity/geographical diversification but tempered by elevated valuations, Bourse maintains a MARKETWEIGHT rating on AMCL.

GraceKennedy Limited (GKC)

GraceKennedy Limited (GKC) reported Earnings per Share (EPS) of TT$0.28 for the nine months ended September 30th, 2024, an increase of 11.2% over the corresponding period in 9M2023.

Revenue from Products and Services increased by 6.9%, moving from TT$4.83B to TT$5.17B, while Interest Revenue grew by 18.1%, reaching TT$218.5M. As a result, Total Revenue for 9M2024 increased by 7.3%, reaching TT$5.38B, compared to TT$5.02B in 9M2023. Direct and Operating Expenses rose to TT$5.10B, and Net Impairment Losses on Financial Assets grew by 4.6% to TT$15.5M, contributing to a 7.4% increase in Total Expenses, up from TT$4.76B in the prior period. GKC’s Profit from Operations grew by 10.4%, increasing from TT$377.7M to TT$417.0M in 9M2024. Interest Income from Non-Financial Services surged by 34.5% year-on-year (YoY), while Interest Expense from Non-Financial Services rose by 22.3%, from TT$51.7M in 9M2023 to TT$63.3M in 9M2024. The Share of Results from Associates and Joint Ventures advanced by 14.1%, reaching TT$31.0M compared to the previous year. Profit Before Tax (PBT) amounted to TT$412.0M, reflecting a 10.3% increase from TT$373.4M in 9M2023. Overall, GKC’s Net Profit Attributable to Owners improved by 11.1%, reaching TT$282.2M, compared to TT$254.1M in the same period of the prior year.

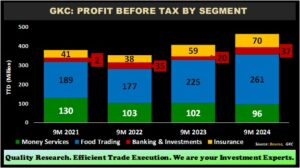

Food Trading Drives PBT

Food Trading, the largest contributor to PBT (56% excluding adjustments), saw a 15.6% increase, moving from TT$225M in 9M2023 to TT$261M in 9M2024. GKC reported that its Grace Foods and Services (GFS), Consumer Brands Limited (CBL), World Brands Limited (WBS), and Hi-Lo Food Stores experienced consistent revenue growth and profitability across both Jamaican and international markets.

GraceKennedy Money Services (GKMS), the second-largest contributor to PBT (21%), experienced a 5.8% year-over-year decline, despite an increase in revenue. The Group’s Insurance Segment, which made up 15% of PBT, improved by 18.6%. This growth was reportedly driven by improvements in GK General Insurance (GKGI), Key Insurance, Allied Insurance Brokers, and Canopy Insurance operations. Banking and Investments, which accounted for 8% of PBT, saw a notable 83.7% increase, driven by strong performance from First Global Bank in Jamaica as well as improved revenue from asset management fees at GK Capital Management.

Margins Improve

GKC’s profitability margins saw slight improvement relative to the prior comparable period. Operating Profit margin edged up from 7.5% in 9M2023 to 7.7% in 9M2024, driven by higher revenues and effective margin management. Likewise, the Profit Before Tax margin increased from 7.4% to 7.7%.

The Bourse View

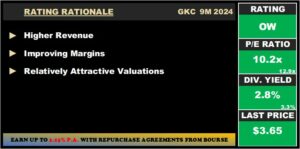

At a current price of $3.65, GKC trades at a P/E ratio of 10.2 times, below the Conglomerate Sector average of 12.9 times. The stock offers investors a trailing dividend yield of 2.8%, below the sector average of 3.3%. The Group announced an interim dividend of TT$0.03, payable to shareholders on December 16th, 2024. GKC’s share buy-back program, which involves the repurchase of up to 1% of GKC shares in issue for over a period of one year is scheduled to end November 2024.

The Group plans to maintain its growth strategy through inorganic opportunities, while also focusing on cost control measures within its current operations. On the basis of revenue growth and improving margins, aided by continued attractive valuations, Bourse maintains an OVERWEIGHT rating on GKC.

“This document has been prepared by Bourse Securities Limited, (“Bourse”), for information purposes only. The production of this publication is not to in any way establish an offer or solicit for the subscription, purchase or sale of any of the securities stated herein to US persons or to contradict any laws of jurisdictions which would interpret our research to be an offer. Any trade in securities recommended herein is done subject to the fact that Bourse, its subsidiaries and/or affiliates have or may have specific or potential conflicts of interest in respect of the security or the issuer of the security, including those arising from (i) trading or dealing in certain securities and acting as an investment advisor; (ii) holding of securities of the issuer as beneficial owner; (iii) having benefitted, benefitting or to benefit from compensation arrangements; (iv) acting as underwriter in any distribution of securities of the issuer in the three years immediately preceding this document; or (v) having direct or indirect financial or other interest in the security or the issuer of the security. Investors are advised accordingly. Neither Bourse nor any of its subsidiaries, affiliates directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses arising from the use of this document or its contents or reliance on the information contained herein. Bourse does not guarantee the accuracy or completeness of the information in this document, which may have been obtained from or is based upon trade and statistical services or other third-party sources. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.”